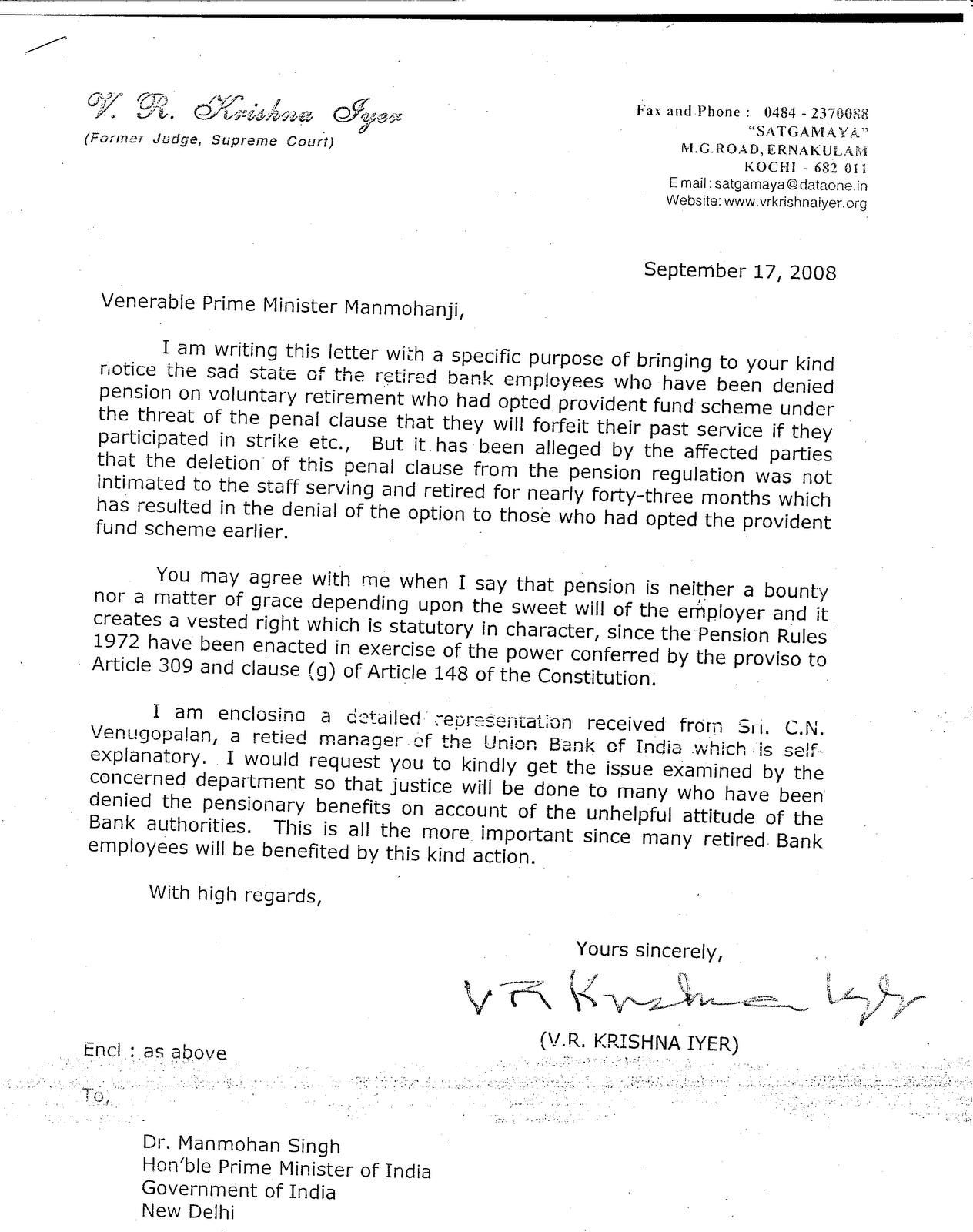

Unions have worked hard(ly) to resolve the burning issues of members and past members who have paid them subscriptions regularly till retirement.

When Pension Scheme came some of them sent wrong signals to members stating that CPF would be beneficial.

When the Final Pension Scheme infused in it the clause providing for forfeiture of entire past services for participation in strike, bank men could not join the scheme lest they would lose CPF as also Pension benefit.

When the clause was scrapped in February, 1999, at the behest of Unions, they did not secure with it a chance for Fresh option which was a legitimate and legal entitlement of all those stayed away when the penal clause was present.

Majority did not get an option under the Pension Scheme that is now in force ( i.e. sans the clause providing for forfeiture of service.

Unions did not help any one and drove all victims to Courts to fight the issue futilely and Supreme Court turned down the appeals in 2001

Government and IBA was adamant in their stand and said that no option would be given

Some Unions wanted to ensure that their opponents never get a chance to opt for Pension again

During the course of 8th Bipartite Settlement Unions sold out the rights of employees altogether in 1995by agreeing with IBA not to open the Pension Issue again.

When the issue surfaced again Unions worked under pressure only and reluctantly fought for fresh option

When a MOU was reached on 25th February, 2008 to settle the Pension Issue logically within 90 days from then, Unions again remained non-performing and allowed IBA to mix the item with wage revision. They added to the hardships of the retired for more than another two years

When it was finally agreed on 27 November, 2009 to five final shape to things within 90 days, then also no interest is evinced to stick to the time frame

Even as things are prolonging beyond 100 days, they say that there is positive outcome.

You be the better judges

C N Venugopalan ceeyenvee at gmail.com

Tuesday, March 16, 2010

Wednesday, December 30, 2009

Pay Hike in Banks - Fair or Not

C N Venugopalan

Ex- Manager, Union Bank of India

“ Nandanam”

Kesari Junction

North Paravoor

Kerala – 683 513

Phone No. 0484 2447994 Mobile: 9447747994

No.20091230 30th December, 2009

The Editor,

Business Line.

Bank Men and Wage hike

The IBA recently settled a pay hike of 17.50 percent and a fresh option for bank men, including the retired who stayed away from the scheme when it contained a penal clause. Bank unions blow the trumpet saying that the percentage of wage hike is the highest one ever secured. The statistically precise statement becomes quite unacceptable in the context of the 40 percent pay hike given to five days working government employees in the pre-election phase when the six days working bankers are settled for 17.50 percent, which is 56.25 percent less than the pay hike to the former.

Pension Option is a benefit already given in 1995 and later denied unlawfully to majority of employees. The final and irrevocable options of certain employees were revoked and others who could not opt when the scheme contained the penal clause were not given a fresh chance when the clause was deleted in 1999. Unions and directors representing officers and workmen remained mute spectators while the fundamental right of the people they represented was taken away. Bipartite Settlement inked in 2005 stated that the issue of fresh option cannot be reopened. Retired, who were victims were driven to courts and the apex court that heard appeals rejected the plea of the bank men in 2001. Government too took a negative stand that fresh option can not be considered at any rate causing hardship to the retired for years.

Even as public sector banks ( excepting State Bank of Saurashtra and State Bank of Indore whose data were not available) made incremental profits of Rs. 32,148.77 Crores for past three years over the 2006 level, IBA worked out a deficit of Rs.1800 Crores for meeting the Pension burden asking the employees to share this 30 percent of the identified liability. The incremental profit of 13 prominent private sector banks for identical period stood at Rs. 19,486.14 Crores. The hike in interest income of the PSBs was Rs. 1,19,919.63 Crores and that of the private sector banks was Rs. 75,780.05 Crores. Spurt in profits and interest income, makes the demand of IBA on the employees to share a portion of the Pension Burden a real plight. Want of financial muscles to bear legitimate establishment expenditure proves as a mere extenuation while analyzing facts and figures.

The Agricultural Debt waiver in 2008 came to Rs.70,000 Crores and other normal write off during the past three years stood at about Rs.25,000 Crores. It takes any Indian to utter surprise when banks which could splendidly bear the burnt of the Rs.95000 Crores on write off find it difficult to extend a reasonable package to the workforce and make a foul bargain for Rs.1,800 Crores for paying the pension.

Pension Regulations have specifically excluded the resigned employees from its purview albeit possessing the prescribed minimum service qualifying for pension. Mode of exit ought to be immaterial and Pension Scheme has to be fine tuned to encompass resigned too when banks are paying pension to VRS retirees who were given a special package for quitting employment. Resignation is the purest form of Voluntary Retirement embraced voluntarily whereas the VRS is a scheme of induced retirement through special incentives offered.

The Minister of Finance and members of Parliament who have taken oath in the name of the Constitution of the country consenting to treat identical people equally will be at a default if they shut their eyes before realities and fail to extend uniform treatment to bank men of all sort. The fact that Bank employees take their salaries from the profits banks make and not from the exchequer should also be taken care of while settling their deal vis-à-vis government employees.

Yours faithfully,

C N Venugopalan

Supporting data testifying the facts enclosed

Supporting data

Profits of Public Sector Banks & SBI group

PROFITS Rs. Crores

March March March March March

2005 2006 2007 2008 2009

PNB 2707.21 2874.77 3230.64 4006.24 5744.35

BOI 340.05 701.44 1123.17 2009.4 3007.35

UBI 719.06 675.16 845.39 1387.03 1726.55

CBI 357.41 257.42 498.01 550.16 571.24

Canara Bank 1109.51 1343.22 1420.81 1565.01 2072.42

IOB 651.36 783.34 1008.43 1202.34 1325.79

UCO Bank 345.65 196.65 316.1 412.16 557.72

Syndicate Bank 402.90 536.50 716.05 848.06 912.82

Allahabad Bank 541.79 706.13 750.14 974.74 768.6

Vijaya Bank 380.57 126.88 331.34 361.28 262.48

BOM 177.12 50.79 271.84 328.39 375.17

Corporation Bank 402.16 444.46 536.15 734.99 892.77

Indian Bank 408.49 504.48 759.77 1008.74 1245.32

Dena Bank 61.00 72.99 201.56 359.79 422.66

BOB 676.84 826.96 1026.47 1435.52 2227.2

Andhra bank 520.1 485.5 537.9 575.57 653.05

OBC 760.81 803.16 826.81 840.94 905.42

SBM 206.26 216.72 249.23 318.85 336.91

SBH 226.49 301.4 427.05 505.5 615.81

SBI 4304.52 4406.67 4541.31 6769.12 9121.24

SBT 247.13 258.68 326.28 386.11 607.84

SBS

SBBJ 205.65 145.03 305.8 315 403.45

SBP 287.07 303.11 366.53 413.73 531.54

State Bank of Indore

16039.15 17021.46 20616.78 27308.67 35287.70

2006 Profits 17021.46 17021.46 17021.46

Incremental profit 3595.32 10287.21 18266.24

Total Increase from 2006 level 32148.77

Profits of selected private sector banks

Rs. Crores

Name of Bank March March March March March

2005 2006 2007 2008 2009

Federal Bank 90.09 225.21 292.73 368.05 500.49

South Indian Bank 8.70 50.90 104.12 154.32 194.75

Axis Bank 334.58 485.08 659.03 1071.03 1815.36

ICICI Bank 2005.20 2540.07 3110.22 4157.73 3758.13

IDBI Bank 307.26 560.89 630.31 729.45 858.53

HDFC Bank 665.56 870.78 1141.45 1590.18 2244.95

City Union Bank 233.16 256.10 331.49 446.69 616.44

J & K Bank 1006.89 1170.48 1386.47 1954.76 2374.91

Karnataka Bank 542.14 754.36 934.92 1213.43 1490.39

IndusInd Bank 728.67 706.28 1092.10 1436.13 1621.58

Yes Bank -10.08 89.42 344.80 926.05 1523.03

DLB -21.60 9.51 16.14 28.46 57.45

Bk of Rajastan 296.76 278.34 475.05 779.36 1047.92

6187.33 7997.42 10518.83 14855.64 18103.93

2006 Profits 7997.42 7997.42 7997.42

Incremental profit 2521.41 6858.22 10106.51

Total Increase from 2006 level 19486.14

Interest Income of Public Sector Banks

March March March March March

2005 2006 2007 2008 2009

PNB 4453.11 4917.39 6022.91 8730.86 12295.30

BOI 3794.64 4396.72 5739.86 8125.95 10848.45

UBI 2905.24 3489.43 4591.96 6360.95 8075.81

CBI 2829.93 3005.51 3759.79 5772.48 8226.72

Canara Bank 4421.50 5130.01 7337.73 10662.94 12401.24

IOB 2095.53 2339.10 3721.27 5288.79 6771.81

UCO Bank 818.66 852.10 944.75 953.95 1201.62

Syndicate Bk 2063.80 2169.55 3890.02 5833.56 6977.60

Allahabad Bank 1072.62 1024.15 1099.91 1479.51 1901.15

Vijaya bank 1109.77 1339.02 1751.16 3058.42 4113.02

BOM 1486.04 1502.90 1627.84 2311.79 3035.03

Corporation Bank 1120.42 1399.66 2052.37 3073.24 4376.37

Indian Bank 1567.00 1854.34 2412.62 3159.08 4221.82

Dena Bank 1038.58 1037.46 1263.16 1817.14 2383.07

BOB 3452.15 3875.09 5426.56 7901.67 9968.17

Andhra bank 1204.42 1505.39 1897.79 2870.00 3747.71

OBC 2048.22 2513.85 3473.58 5156.17 6859.97

SBM 623.03 735.09 1092.91 1732.10 2409.02

SBH 1268.64 1319.51 1654.55 2134.53 4242.71

SBI 18483.38 20159.29 23436.82 31929.08 42915.29

SBT 1112.16 1343.49 1698.44 2476.82 2840.60

SBS

SBBJ 871.98 972.88 1435.42 2112.98 2707.06

SBP 1156.96 1464.87 2059.63 3419.62 4676.32

37481.63 42351.67 57013.28 82556.5 107404.86

2006 Income 42351.67 42351.67 42351.67

Incremental Income 14661.61 40204.83 65053.19

Total Increase from 2006 level 119919.63

Interest Income of Private Sector Banks

Rs, Crores

March March March March March

Name of Bank 2005 2006 2007 2008 2009

Federal Bank 688.75 836.73 1084.96 1647.43 1999.92

South Indian Bank 452.07 451.14 609.09 915.10 1164.04

Axis Bank 1192.98 1810.56 2993.32 4419.96 7149.27

ICICI Bank 6570.89 9597.45 16358.5 23484.24 22725.93

IDBI Bank 2467.87 5000.82 5687.49 7364.41 10305.72

HDFC Bank 1315.56 1929.50 3179.45 4887.12 8911.10

City Union Bank 179.84 186.61 232.56 396.18 561.83

J & K Bank 952.99 1042.53 1131.48 1623.79 1987.86

Karnataka Bank 523.04 652.07 836.39 1101.71 1443.83

IndusInd Bank 718.89 873.19 1228.85 1579.86 1850.44

Yes Bank 11.85 104.72 416.26 974.11 1492.14

DLB 119.06 126.89 149.77 213.50 286.80

Bk of Rajastan 308.91 317.06 439.4 735.60 998.45

15502.7 22929.27 34347.52 49343.01 60877.33

2006 Profits 22929.27 22929.27 22929.27

Incremental profit 11418.25 26413.74 37948.06

Total Increase from 2006 level 75780.05

Ex- Manager, Union Bank of India

“ Nandanam”

Kesari Junction

North Paravoor

Kerala – 683 513

Phone No. 0484 2447994 Mobile: 9447747994

No.20091230 30th December, 2009

The Editor,

Business Line.

Bank Men and Wage hike

The IBA recently settled a pay hike of 17.50 percent and a fresh option for bank men, including the retired who stayed away from the scheme when it contained a penal clause. Bank unions blow the trumpet saying that the percentage of wage hike is the highest one ever secured. The statistically precise statement becomes quite unacceptable in the context of the 40 percent pay hike given to five days working government employees in the pre-election phase when the six days working bankers are settled for 17.50 percent, which is 56.25 percent less than the pay hike to the former.

Pension Option is a benefit already given in 1995 and later denied unlawfully to majority of employees. The final and irrevocable options of certain employees were revoked and others who could not opt when the scheme contained the penal clause were not given a fresh chance when the clause was deleted in 1999. Unions and directors representing officers and workmen remained mute spectators while the fundamental right of the people they represented was taken away. Bipartite Settlement inked in 2005 stated that the issue of fresh option cannot be reopened. Retired, who were victims were driven to courts and the apex court that heard appeals rejected the plea of the bank men in 2001. Government too took a negative stand that fresh option can not be considered at any rate causing hardship to the retired for years.

Even as public sector banks ( excepting State Bank of Saurashtra and State Bank of Indore whose data were not available) made incremental profits of Rs. 32,148.77 Crores for past three years over the 2006 level, IBA worked out a deficit of Rs.1800 Crores for meeting the Pension burden asking the employees to share this 30 percent of the identified liability. The incremental profit of 13 prominent private sector banks for identical period stood at Rs. 19,486.14 Crores. The hike in interest income of the PSBs was Rs. 1,19,919.63 Crores and that of the private sector banks was Rs. 75,780.05 Crores. Spurt in profits and interest income, makes the demand of IBA on the employees to share a portion of the Pension Burden a real plight. Want of financial muscles to bear legitimate establishment expenditure proves as a mere extenuation while analyzing facts and figures.

The Agricultural Debt waiver in 2008 came to Rs.70,000 Crores and other normal write off during the past three years stood at about Rs.25,000 Crores. It takes any Indian to utter surprise when banks which could splendidly bear the burnt of the Rs.95000 Crores on write off find it difficult to extend a reasonable package to the workforce and make a foul bargain for Rs.1,800 Crores for paying the pension.

Pension Regulations have specifically excluded the resigned employees from its purview albeit possessing the prescribed minimum service qualifying for pension. Mode of exit ought to be immaterial and Pension Scheme has to be fine tuned to encompass resigned too when banks are paying pension to VRS retirees who were given a special package for quitting employment. Resignation is the purest form of Voluntary Retirement embraced voluntarily whereas the VRS is a scheme of induced retirement through special incentives offered.

The Minister of Finance and members of Parliament who have taken oath in the name of the Constitution of the country consenting to treat identical people equally will be at a default if they shut their eyes before realities and fail to extend uniform treatment to bank men of all sort. The fact that Bank employees take their salaries from the profits banks make and not from the exchequer should also be taken care of while settling their deal vis-à-vis government employees.

Yours faithfully,

C N Venugopalan

Supporting data testifying the facts enclosed

Supporting data

Profits of Public Sector Banks & SBI group

PROFITS Rs. Crores

March March March March March

2005 2006 2007 2008 2009

PNB 2707.21 2874.77 3230.64 4006.24 5744.35

BOI 340.05 701.44 1123.17 2009.4 3007.35

UBI 719.06 675.16 845.39 1387.03 1726.55

CBI 357.41 257.42 498.01 550.16 571.24

Canara Bank 1109.51 1343.22 1420.81 1565.01 2072.42

IOB 651.36 783.34 1008.43 1202.34 1325.79

UCO Bank 345.65 196.65 316.1 412.16 557.72

Syndicate Bank 402.90 536.50 716.05 848.06 912.82

Allahabad Bank 541.79 706.13 750.14 974.74 768.6

Vijaya Bank 380.57 126.88 331.34 361.28 262.48

BOM 177.12 50.79 271.84 328.39 375.17

Corporation Bank 402.16 444.46 536.15 734.99 892.77

Indian Bank 408.49 504.48 759.77 1008.74 1245.32

Dena Bank 61.00 72.99 201.56 359.79 422.66

BOB 676.84 826.96 1026.47 1435.52 2227.2

Andhra bank 520.1 485.5 537.9 575.57 653.05

OBC 760.81 803.16 826.81 840.94 905.42

SBM 206.26 216.72 249.23 318.85 336.91

SBH 226.49 301.4 427.05 505.5 615.81

SBI 4304.52 4406.67 4541.31 6769.12 9121.24

SBT 247.13 258.68 326.28 386.11 607.84

SBS

SBBJ 205.65 145.03 305.8 315 403.45

SBP 287.07 303.11 366.53 413.73 531.54

State Bank of Indore

16039.15 17021.46 20616.78 27308.67 35287.70

2006 Profits 17021.46 17021.46 17021.46

Incremental profit 3595.32 10287.21 18266.24

Total Increase from 2006 level 32148.77

Profits of selected private sector banks

Rs. Crores

Name of Bank March March March March March

2005 2006 2007 2008 2009

Federal Bank 90.09 225.21 292.73 368.05 500.49

South Indian Bank 8.70 50.90 104.12 154.32 194.75

Axis Bank 334.58 485.08 659.03 1071.03 1815.36

ICICI Bank 2005.20 2540.07 3110.22 4157.73 3758.13

IDBI Bank 307.26 560.89 630.31 729.45 858.53

HDFC Bank 665.56 870.78 1141.45 1590.18 2244.95

City Union Bank 233.16 256.10 331.49 446.69 616.44

J & K Bank 1006.89 1170.48 1386.47 1954.76 2374.91

Karnataka Bank 542.14 754.36 934.92 1213.43 1490.39

IndusInd Bank 728.67 706.28 1092.10 1436.13 1621.58

Yes Bank -10.08 89.42 344.80 926.05 1523.03

DLB -21.60 9.51 16.14 28.46 57.45

Bk of Rajastan 296.76 278.34 475.05 779.36 1047.92

6187.33 7997.42 10518.83 14855.64 18103.93

2006 Profits 7997.42 7997.42 7997.42

Incremental profit 2521.41 6858.22 10106.51

Total Increase from 2006 level 19486.14

Interest Income of Public Sector Banks

March March March March March

2005 2006 2007 2008 2009

PNB 4453.11 4917.39 6022.91 8730.86 12295.30

BOI 3794.64 4396.72 5739.86 8125.95 10848.45

UBI 2905.24 3489.43 4591.96 6360.95 8075.81

CBI 2829.93 3005.51 3759.79 5772.48 8226.72

Canara Bank 4421.50 5130.01 7337.73 10662.94 12401.24

IOB 2095.53 2339.10 3721.27 5288.79 6771.81

UCO Bank 818.66 852.10 944.75 953.95 1201.62

Syndicate Bk 2063.80 2169.55 3890.02 5833.56 6977.60

Allahabad Bank 1072.62 1024.15 1099.91 1479.51 1901.15

Vijaya bank 1109.77 1339.02 1751.16 3058.42 4113.02

BOM 1486.04 1502.90 1627.84 2311.79 3035.03

Corporation Bank 1120.42 1399.66 2052.37 3073.24 4376.37

Indian Bank 1567.00 1854.34 2412.62 3159.08 4221.82

Dena Bank 1038.58 1037.46 1263.16 1817.14 2383.07

BOB 3452.15 3875.09 5426.56 7901.67 9968.17

Andhra bank 1204.42 1505.39 1897.79 2870.00 3747.71

OBC 2048.22 2513.85 3473.58 5156.17 6859.97

SBM 623.03 735.09 1092.91 1732.10 2409.02

SBH 1268.64 1319.51 1654.55 2134.53 4242.71

SBI 18483.38 20159.29 23436.82 31929.08 42915.29

SBT 1112.16 1343.49 1698.44 2476.82 2840.60

SBS

SBBJ 871.98 972.88 1435.42 2112.98 2707.06

SBP 1156.96 1464.87 2059.63 3419.62 4676.32

37481.63 42351.67 57013.28 82556.5 107404.86

2006 Income 42351.67 42351.67 42351.67

Incremental Income 14661.61 40204.83 65053.19

Total Increase from 2006 level 119919.63

Interest Income of Private Sector Banks

Rs, Crores

March March March March March

Name of Bank 2005 2006 2007 2008 2009

Federal Bank 688.75 836.73 1084.96 1647.43 1999.92

South Indian Bank 452.07 451.14 609.09 915.10 1164.04

Axis Bank 1192.98 1810.56 2993.32 4419.96 7149.27

ICICI Bank 6570.89 9597.45 16358.5 23484.24 22725.93

IDBI Bank 2467.87 5000.82 5687.49 7364.41 10305.72

HDFC Bank 1315.56 1929.50 3179.45 4887.12 8911.10

City Union Bank 179.84 186.61 232.56 396.18 561.83

J & K Bank 952.99 1042.53 1131.48 1623.79 1987.86

Karnataka Bank 523.04 652.07 836.39 1101.71 1443.83

IndusInd Bank 718.89 873.19 1228.85 1579.86 1850.44

Yes Bank 11.85 104.72 416.26 974.11 1492.14

DLB 119.06 126.89 149.77 213.50 286.80

Bk of Rajastan 308.91 317.06 439.4 735.60 998.45

15502.7 22929.27 34347.52 49343.01 60877.33

2006 Profits 22929.27 22929.27 22929.27

Incremental profit 11418.25 26413.74 37948.06

Total Increase from 2006 level 75780.05

Friday, December 18, 2009

Fresh Option for Pension in Banks - Unveiling the truth

Unveiling truth about Pension Option afresh

• While Pension Scheme was introduced in 1995 some unions advocated it for all while others propounded that CPF would be beneficial and prevented many from exercising option

• The former wanted to ensure that those who did take their advice never get a chance again

• The latter remained firm on their stand and befooled members saying that CPF was still beneficial

• Both went in parallel lines that would never meet

• Many employees could not join the Scheme because of the infusion of the forfeiture of service clause in the final Pension Regulations

• Some who had opted in terms of draft Regulations quit the scheme when the forfeiture of service clause was infused when banks permitted revocation

• Revocation was null and void since the draft and Government sanctioned Regulations stated that “option once exercised shall be final and irrevocable”

• Banks did not extend and unions did not procure a fresh option to those who could not opt earlier when the penal clause remained in the Regulations upon deletion of the penal clause on 27th February, 1999 which created a legal obligation to do so

• Unions drove all those retired to various courts without extending any help and suits and appeals decided against employees created a formidable obstacle which could not be cleared easily

• Government categorically stated that it would not open the issue of Option again.

• Unions agreed in 2005 with IBA not to open the issue again, virtually selling out the fundamental right.

• Even as option was a legally vested right of all employees in 1999, Unions joined hands with managements and did not perform for it

• Pension Option became a shattered dream of bank men and a stale item with the passage of time and vanished from the charter of demand of all unions by 2005

• My vehement criticisms and a circular letter (dated 10th January, 2006) sent on all India bases explaining the lapse of the Unions and illegality IBA perpetrated brought the issue to lime light once again. But for the prodding and propulsion I did, the issue buried for would never have surfaced out again

• After a series of agitations, a MOU was signed on 25th February, 2008 between IBA and UFBU to the effect that the issue would be settled within three months.

• The time frame of the MOU of 25th February, 2008 was breached as Unions did not evince any interest in concluding things within the time frame.

• The issue got mixed up with wage talks and prolonged to add to the hardships of those retired. Working people suffered for ever since IBA made a foul bargain in the name of Pension burden by offering a low hike to bank employees who toil for six days when government employees who work merely for five days got a hike of 40 percent.

• Unions once again partially sold out the rights of bank men by agreeing to 70:30 sharing formula for the pension burden.

• Even as a final agreement was reached on 7th August 2009 on 17.50 percent hike and Pension Option, the next round of sitting could be arranged only on 27th November, 2009 after lapsing three and a half months

Those who opposed a fresh option tooth and nail now say that they achieved the “second option” when none has got the first option as per the Regulations sans forfeiture of service clause

• While Pension Scheme was introduced in 1995 some unions advocated it for all while others propounded that CPF would be beneficial and prevented many from exercising option

• The former wanted to ensure that those who did take their advice never get a chance again

• The latter remained firm on their stand and befooled members saying that CPF was still beneficial

• Both went in parallel lines that would never meet

• Many employees could not join the Scheme because of the infusion of the forfeiture of service clause in the final Pension Regulations

• Some who had opted in terms of draft Regulations quit the scheme when the forfeiture of service clause was infused when banks permitted revocation

• Revocation was null and void since the draft and Government sanctioned Regulations stated that “option once exercised shall be final and irrevocable”

• Banks did not extend and unions did not procure a fresh option to those who could not opt earlier when the penal clause remained in the Regulations upon deletion of the penal clause on 27th February, 1999 which created a legal obligation to do so

• Unions drove all those retired to various courts without extending any help and suits and appeals decided against employees created a formidable obstacle which could not be cleared easily

• Government categorically stated that it would not open the issue of Option again.

• Unions agreed in 2005 with IBA not to open the issue again, virtually selling out the fundamental right.

• Even as option was a legally vested right of all employees in 1999, Unions joined hands with managements and did not perform for it

• Pension Option became a shattered dream of bank men and a stale item with the passage of time and vanished from the charter of demand of all unions by 2005

• My vehement criticisms and a circular letter (dated 10th January, 2006) sent on all India bases explaining the lapse of the Unions and illegality IBA perpetrated brought the issue to lime light once again. But for the prodding and propulsion I did, the issue buried for would never have surfaced out again

• After a series of agitations, a MOU was signed on 25th February, 2008 between IBA and UFBU to the effect that the issue would be settled within three months.

• The time frame of the MOU of 25th February, 2008 was breached as Unions did not evince any interest in concluding things within the time frame.

• The issue got mixed up with wage talks and prolonged to add to the hardships of those retired. Working people suffered for ever since IBA made a foul bargain in the name of Pension burden by offering a low hike to bank employees who toil for six days when government employees who work merely for five days got a hike of 40 percent.

• Unions once again partially sold out the rights of bank men by agreeing to 70:30 sharing formula for the pension burden.

• Even as a final agreement was reached on 7th August 2009 on 17.50 percent hike and Pension Option, the next round of sitting could be arranged only on 27th November, 2009 after lapsing three and a half months

Those who opposed a fresh option tooth and nail now say that they achieved the “second option” when none has got the first option as per the Regulations sans forfeiture of service clause

Wednesday, December 9, 2009

Pension Burden - 30 percent Recovery from Wage Hike

C N Venugopalan

Ex- Manager, Union Bank of India

“ Nandanam”

Kesari Junction

North Paravoor

Kerala – 683 513

Phone No. 0484 2447994 Mobile: 9447747994

No. 20091207 07th December, 2009

Smt. Jayanthi Natarajan,

Member of the Parliament and Chairperson, Grievances Committee,

Government of India, New Delhi

Madam,

Pension Option and Wage Pact in Banks

I am extremely glad to know that as a result of the key role you played, IBA and UFBU concluded the captioned items. Thank you for everything on behalf of the retired employees and on my personal behalf.

I thought it worthwhile to bring to your information the following points in the context of the IBA making the employees share 30 percent of the Pension burden out of the wage hike sanctioned:

Eighteen listed Public Sector Banks in India (excepting banks that are not listed) showed the below mentioned profits during the past five years:

March March March March March Rs. Crores

2005 2006 2007 2008 2009

Punjab National Bank 2707.21 2874.77 3230.64 4006.24 5744.35

Bank of India 340.05 701.44 1123.17 2009.40 3007.35

Union Bank of India 719.06 675.16 845.39 1387.03 1726.55

Central Bank of India 357.41 257.42 498.01 550.16 571.24

Canara Bank 1109.51 1343.22 1420.81 1565.01 2072.42

Indian Overseas Bank 651.36 783.34 1008.43 1202.34 1325.79

UCO Bank 345.65 196.65 316.10 412.16 557.72

Syndicate Bank 402.90 536.50 716.05 848.06 912.82

Allahabad Bank 541.79 706.13 750.14 974.74 768.60

Vijaya Bank 380.57 126.88 331.34 361.28 262.48

Bank of Maharashtra 177.12 50.79 271.84 328.39 375.17

Corporation Bank 402.16 444.46 536.15 734.99 892.77

Indian Bank 408.49 504.48 759.77 1008.74 1245.32

Dena Bank 61.00 72.99 201.56 359.79 422.66

Bank of Baroda 676.84 826.96 1026.47 1435.52 2227.20

Andhra bank 520.10 485.50 537.90 575.57 653.05

Oriental Bank of Commerce 760.81 803.16 826.81 840.94 905.42

Total

10562.03 11389.85 14400.58 18600.36 23670.91

Profit above March 2006 level (Incremental Profit)

3010.73 7210.51 12281.06

Total Profit hike for all the three years 22502.30

Even as they made incremental profits of Rs.22, 502 Crores + (data for 2 Nationalised banks and six subsidiaries of SBI not included) over the March 2006 IBA has made employees to share a burden of Rs.1800 Crores towards Pension. During the past three years the loan waiver by banks was to the extent of Rs.25,000 Crores which was in addition to the Agricultural waiver of Rs.60,000 Crores. While they could easily accommodate Rs.85000 Crores on write off, banks were pleading paucity of funds to meet the Pension burden in spite of the progressive and cumulative Net Profit figures.

During 2002 -2006 period public sector banks standing under the common umbrella of IBA were competing with and pulling the legs of one another sans any business ethics. They were caught with “take over mania” and snatched away big loan accounts from counterparts using the lethal weapon of interest rate, offering concessions to big and potential people in the deregulated interest regime RBI permitted. The exercise was to add to the cosmetics of the key men by broadening the lending base. RBI remained cool as if it was watching a cricket game and the life blood of banks oozed out like anything. Key men who drew large emoluments and perks and whose responsibility it was to strengthen banks were debilitating them. History tells that in spite of the close surveillance of banks by RBI keeping its men as directors on bank boards, even a public sector bank viz. New Bank of India vanished into obscurity. RBI emerged into the picture only when a catastrophe arose, merged that entity with some strong bank, saved its face and went back to the barrack.

When I mooted vehement criticisms to RBI, MOF etc., against the undesirable tendency that damaged the banking system, the interest concessions were abolished to a great extent in August, 2006 and it is after this period all banks in India started making progressive profits. A major portion of the cumulative profits of Rs.22502-30 Crores can rightly be attributed to my work done remaining outside the banking system for no compensation. I am also denied the Pension Payable to me on my Voluntary Retirement from Union Bank of India on 20th April, 2001 in spite of the yeoman services done extraordinary contribution subsequently made to banking system.

The ninth bipartite settlement encompassing the Pension Option is totally a ridiculous thing. All employees on rolls of the banks in 1995 are entitled to a fresh option and it is a legally vested and already sanctioned item. In 1995 the Government sanctioned Pension Scheme ( adopted by boards of Banks too) was offered keeping therein a draconian clause to the effect that if any employee participated in a strike banks could forfeit his entire past service. Joining Pension scheme through exercising an option within the set time frame entailed surrender to the Bank’s Pension Fund the entire CPF (employer’s share) standing to his credit and one had to secure a minimum qualifying service of 20 years to be eligible for Pension. It meant that in case the bank forfeited the entire past services of an employee and he fails to secure 20 years’ service afterwards, he would lose the existing benefit of CPF as also Pension. This prevented majority of employees from opting for Pension.

When the aforesaid penal clause was deleted from the Pension Regulations on 27th February, 1999, banks did not extend a chance of fresh option to those who could not opt for it because of the presence of the deleted clause earlier. Moreover, they kept the information in camera without reaching the employees by giving mere gazette publication of the amendment, in total deviation of the normal practice of circulating all amendments among employees beforehand. The amendment vested with each employee on rolls of banks in 1995 a right to Pension Option afresh which banks illegally denied. Neither the Unions nor the Directors representing employees demand and obtain the vested right.

Before publishing the Government sanctioned final Scheme, a draft was published earlier which too had called for options within a time frame. Several employees who opted in terms thereof wanted to take exit when the clause providing for forfeiture of service was infused into Final Regulations. After publishing Final Regulations, banks came with an offer permitting any one (who opted in response to draft Regulations) to take exit from the scheme by submitting his request. This they did upon mere advice from the IBA which had no authority exceeding that of the Board of the Bank or the Government which sanctioned the scheme. Banks revoked the options of several employees in spite of the fact that the Regulations contained no procedure or provision for revocation of an exercised option and both the draft as also the final Regulations stated that “an option, once exercised shall be final and irrevocable”. The revocation banks contemplated is thus illegal and void. I am not paid Pension though the option I exercised on 30 09 1994 is of a final character.

Trade Unions that regularly raised tolls from members failed to protect the legally vested rights of the employees. Banks pleaded inability to pay the legitimate establishment expenditure which courts had stated as an inalienable right of the employee akin to fundamental rights of a citizen earned through relentless service and not as a charity doled out to the retired employee at the sweet will of the employer. Banks which originated and function entirely on the premises of some law or other were showing utter disregard to the rules and regulations they themselves framed. Can any banker say what banks would have done if every one had opted for Pension when initially offered? They had money to spend extravagantly but they lacked funds to meet genuine establishment expenditure legally payable. Unions aided and abetted the process without claiming the already sanctioned and legally vested social security benefit of members.

Those retired during the period from 1995 to date without Pension Option were stranded in life and Unions drove them to Courts. In 2001, the three judge bench of SC rejected intervention and turned down the appeals, closing the matter. Government had also categorically stated that fresh option would not be granted. The Unions differed among themselves and surrendered the rights of employees. Those who initially advised all employees to opt for Pension when the scheme was commissioned wanted to make sure that their rivals who said that CPF would be beneficial never get a chance to opt again. The latter stuck to their stand that they were right in recommending CPF even on knowing facts to be otherwise. They went like parallel lines that would never meet. Pension Option vanished from the agenda or demand list of all Unions and their agitation programs for years together and it became a stale one by 2001. Ultimately in December, 2005, Unions agreed with IBA during the course of 8th Bipartite settlement not to open the issue again, thereby selling out the cardinal rights of the employees for ever. A fresh option for Pension became a shattered dream of the bank employees.

Right from 2001 April, I had taken up the matter with several authorities but with no avail. On 1st April, 2003, I had filed a petition nearly three years (not heard even now). Knowing that Court would not be of assistance to the victims, I issued an all India Circular among bank employees stating how and why they were entitled to fresh option and showing the inertia of the Unions in the matter. Thousands of e-mails were sent to different bank offices and ultimately the Unions had no alternative other than to perform on it. This is how Pension Option once again figured in the agenda of agitations and ultimately became a reality.

When three or four agitations took place there arose a MOU on 25th February, 2008 between IBA and UFBU to logically conclude the item within three months from then. Three months, six months, nine months, twelve months and fifteen months passed by on account of lack of interest of Unions. Ultimately the item got mixed up with wage revision giving the banks a chance for making a foul bargain on pay hike in the name of the Pension liability. Pension was an already sanctioned benefit to be extended pursuant to Pension Regulations and not in any way related to wage agreement. The sharing formula of 70:30 by banks and employees (out of proposed wage hike) is also illogical since those retired under VRS as also on superannuation from the Pension segment are already paid regular pension without any contribution. The sharing formula has no legal backing and is an arbitrary and illegal step. Pension is expenditure to be borne by employer and not by employee.

Though Unions differed among themselves and joined hands with bank to deny the legitimate right of the employees for about one and a half decade and put all retired to extreme hardship, both schools of thought are now competing with each to say that each of them redeemed the lost right. In fact they remained non-performing on it and made serious lapses all along. The letters of appreciation I received from people who are not personally known to me testify that my relentless work on the issue for eight years and finally using the unions as my weapon to fight against the IBA has given solace to lakhs of bank men. The banking system is benefited substantially through the huge profits it could make as a result of my work and gets sheen through eradication of the injustice it perpetrated on its work force. Unions also can have a face lift to some extent since they worked for and secured the right for the members though through my prodding and propelling. If they are seasoned and responsible people, they should tender apologies to the members and the retired bank men for having leashed their right for about a decade.

I make an earnest appeal to you to please interfere in the matter and to take up with IBA to settle the Pension Option issue in a befitting manner by giving up the sharing formula and by granting pension option and arrears to all employees including the VRS retirees who are legally entitled to it.

Thanks and Regards,

Yours faithfully,

C N Venugopalan

Ex- Manager, Union Bank of India

“ Nandanam”

Kesari Junction

North Paravoor

Kerala – 683 513

Phone No. 0484 2447994 Mobile: 9447747994

No. 20091207 07th December, 2009

Smt. Jayanthi Natarajan,

Member of the Parliament and Chairperson, Grievances Committee,

Government of India, New Delhi

Madam,

Pension Option and Wage Pact in Banks

I am extremely glad to know that as a result of the key role you played, IBA and UFBU concluded the captioned items. Thank you for everything on behalf of the retired employees and on my personal behalf.

I thought it worthwhile to bring to your information the following points in the context of the IBA making the employees share 30 percent of the Pension burden out of the wage hike sanctioned:

Eighteen listed Public Sector Banks in India (excepting banks that are not listed) showed the below mentioned profits during the past five years:

March March March March March Rs. Crores

2005 2006 2007 2008 2009

Punjab National Bank 2707.21 2874.77 3230.64 4006.24 5744.35

Bank of India 340.05 701.44 1123.17 2009.40 3007.35

Union Bank of India 719.06 675.16 845.39 1387.03 1726.55

Central Bank of India 357.41 257.42 498.01 550.16 571.24

Canara Bank 1109.51 1343.22 1420.81 1565.01 2072.42

Indian Overseas Bank 651.36 783.34 1008.43 1202.34 1325.79

UCO Bank 345.65 196.65 316.10 412.16 557.72

Syndicate Bank 402.90 536.50 716.05 848.06 912.82

Allahabad Bank 541.79 706.13 750.14 974.74 768.60

Vijaya Bank 380.57 126.88 331.34 361.28 262.48

Bank of Maharashtra 177.12 50.79 271.84 328.39 375.17

Corporation Bank 402.16 444.46 536.15 734.99 892.77

Indian Bank 408.49 504.48 759.77 1008.74 1245.32

Dena Bank 61.00 72.99 201.56 359.79 422.66

Bank of Baroda 676.84 826.96 1026.47 1435.52 2227.20

Andhra bank 520.10 485.50 537.90 575.57 653.05

Oriental Bank of Commerce 760.81 803.16 826.81 840.94 905.42

Total

10562.03 11389.85 14400.58 18600.36 23670.91

Profit above March 2006 level (Incremental Profit)

3010.73 7210.51 12281.06

Total Profit hike for all the three years 22502.30

Even as they made incremental profits of Rs.22, 502 Crores + (data for 2 Nationalised banks and six subsidiaries of SBI not included) over the March 2006 IBA has made employees to share a burden of Rs.1800 Crores towards Pension. During the past three years the loan waiver by banks was to the extent of Rs.25,000 Crores which was in addition to the Agricultural waiver of Rs.60,000 Crores. While they could easily accommodate Rs.85000 Crores on write off, banks were pleading paucity of funds to meet the Pension burden in spite of the progressive and cumulative Net Profit figures.

During 2002 -2006 period public sector banks standing under the common umbrella of IBA were competing with and pulling the legs of one another sans any business ethics. They were caught with “take over mania” and snatched away big loan accounts from counterparts using the lethal weapon of interest rate, offering concessions to big and potential people in the deregulated interest regime RBI permitted. The exercise was to add to the cosmetics of the key men by broadening the lending base. RBI remained cool as if it was watching a cricket game and the life blood of banks oozed out like anything. Key men who drew large emoluments and perks and whose responsibility it was to strengthen banks were debilitating them. History tells that in spite of the close surveillance of banks by RBI keeping its men as directors on bank boards, even a public sector bank viz. New Bank of India vanished into obscurity. RBI emerged into the picture only when a catastrophe arose, merged that entity with some strong bank, saved its face and went back to the barrack.

When I mooted vehement criticisms to RBI, MOF etc., against the undesirable tendency that damaged the banking system, the interest concessions were abolished to a great extent in August, 2006 and it is after this period all banks in India started making progressive profits. A major portion of the cumulative profits of Rs.22502-30 Crores can rightly be attributed to my work done remaining outside the banking system for no compensation. I am also denied the Pension Payable to me on my Voluntary Retirement from Union Bank of India on 20th April, 2001 in spite of the yeoman services done extraordinary contribution subsequently made to banking system.

The ninth bipartite settlement encompassing the Pension Option is totally a ridiculous thing. All employees on rolls of the banks in 1995 are entitled to a fresh option and it is a legally vested and already sanctioned item. In 1995 the Government sanctioned Pension Scheme ( adopted by boards of Banks too) was offered keeping therein a draconian clause to the effect that if any employee participated in a strike banks could forfeit his entire past service. Joining Pension scheme through exercising an option within the set time frame entailed surrender to the Bank’s Pension Fund the entire CPF (employer’s share) standing to his credit and one had to secure a minimum qualifying service of 20 years to be eligible for Pension. It meant that in case the bank forfeited the entire past services of an employee and he fails to secure 20 years’ service afterwards, he would lose the existing benefit of CPF as also Pension. This prevented majority of employees from opting for Pension.

When the aforesaid penal clause was deleted from the Pension Regulations on 27th February, 1999, banks did not extend a chance of fresh option to those who could not opt for it because of the presence of the deleted clause earlier. Moreover, they kept the information in camera without reaching the employees by giving mere gazette publication of the amendment, in total deviation of the normal practice of circulating all amendments among employees beforehand. The amendment vested with each employee on rolls of banks in 1995 a right to Pension Option afresh which banks illegally denied. Neither the Unions nor the Directors representing employees demand and obtain the vested right.

Before publishing the Government sanctioned final Scheme, a draft was published earlier which too had called for options within a time frame. Several employees who opted in terms thereof wanted to take exit when the clause providing for forfeiture of service was infused into Final Regulations. After publishing Final Regulations, banks came with an offer permitting any one (who opted in response to draft Regulations) to take exit from the scheme by submitting his request. This they did upon mere advice from the IBA which had no authority exceeding that of the Board of the Bank or the Government which sanctioned the scheme. Banks revoked the options of several employees in spite of the fact that the Regulations contained no procedure or provision for revocation of an exercised option and both the draft as also the final Regulations stated that “an option, once exercised shall be final and irrevocable”. The revocation banks contemplated is thus illegal and void. I am not paid Pension though the option I exercised on 30 09 1994 is of a final character.

Trade Unions that regularly raised tolls from members failed to protect the legally vested rights of the employees. Banks pleaded inability to pay the legitimate establishment expenditure which courts had stated as an inalienable right of the employee akin to fundamental rights of a citizen earned through relentless service and not as a charity doled out to the retired employee at the sweet will of the employer. Banks which originated and function entirely on the premises of some law or other were showing utter disregard to the rules and regulations they themselves framed. Can any banker say what banks would have done if every one had opted for Pension when initially offered? They had money to spend extravagantly but they lacked funds to meet genuine establishment expenditure legally payable. Unions aided and abetted the process without claiming the already sanctioned and legally vested social security benefit of members.

Those retired during the period from 1995 to date without Pension Option were stranded in life and Unions drove them to Courts. In 2001, the three judge bench of SC rejected intervention and turned down the appeals, closing the matter. Government had also categorically stated that fresh option would not be granted. The Unions differed among themselves and surrendered the rights of employees. Those who initially advised all employees to opt for Pension when the scheme was commissioned wanted to make sure that their rivals who said that CPF would be beneficial never get a chance to opt again. The latter stuck to their stand that they were right in recommending CPF even on knowing facts to be otherwise. They went like parallel lines that would never meet. Pension Option vanished from the agenda or demand list of all Unions and their agitation programs for years together and it became a stale one by 2001. Ultimately in December, 2005, Unions agreed with IBA during the course of 8th Bipartite settlement not to open the issue again, thereby selling out the cardinal rights of the employees for ever. A fresh option for Pension became a shattered dream of the bank employees.

Right from 2001 April, I had taken up the matter with several authorities but with no avail. On 1st April, 2003, I had filed a petition nearly three years (not heard even now). Knowing that Court would not be of assistance to the victims, I issued an all India Circular among bank employees stating how and why they were entitled to fresh option and showing the inertia of the Unions in the matter. Thousands of e-mails were sent to different bank offices and ultimately the Unions had no alternative other than to perform on it. This is how Pension Option once again figured in the agenda of agitations and ultimately became a reality.

When three or four agitations took place there arose a MOU on 25th February, 2008 between IBA and UFBU to logically conclude the item within three months from then. Three months, six months, nine months, twelve months and fifteen months passed by on account of lack of interest of Unions. Ultimately the item got mixed up with wage revision giving the banks a chance for making a foul bargain on pay hike in the name of the Pension liability. Pension was an already sanctioned benefit to be extended pursuant to Pension Regulations and not in any way related to wage agreement. The sharing formula of 70:30 by banks and employees (out of proposed wage hike) is also illogical since those retired under VRS as also on superannuation from the Pension segment are already paid regular pension without any contribution. The sharing formula has no legal backing and is an arbitrary and illegal step. Pension is expenditure to be borne by employer and not by employee.

Though Unions differed among themselves and joined hands with bank to deny the legitimate right of the employees for about one and a half decade and put all retired to extreme hardship, both schools of thought are now competing with each to say that each of them redeemed the lost right. In fact they remained non-performing on it and made serious lapses all along. The letters of appreciation I received from people who are not personally known to me testify that my relentless work on the issue for eight years and finally using the unions as my weapon to fight against the IBA has given solace to lakhs of bank men. The banking system is benefited substantially through the huge profits it could make as a result of my work and gets sheen through eradication of the injustice it perpetrated on its work force. Unions also can have a face lift to some extent since they worked for and secured the right for the members though through my prodding and propelling. If they are seasoned and responsible people, they should tender apologies to the members and the retired bank men for having leashed their right for about a decade.

I make an earnest appeal to you to please interfere in the matter and to take up with IBA to settle the Pension Option issue in a befitting manner by giving up the sharing formula and by granting pension option and arrears to all employees including the VRS retirees who are legally entitled to it.

Thanks and Regards,

Yours faithfully,

C N Venugopalan

Sunday, December 6, 2009

banking system comes loaded with fake currency

Dear Comrades,

Banking System fully loaded with Fake Currency

On 2008 March 6 by the then Finance Minister stated as follows

(Financial Express on 7th March, 2007)

The minister added that RBI governor Y V Reddy has told the board that the central bank was “fully geared to support the government in implementing the scheme in a manner that the banking sector will be strengthened, not weakened.”

This is the new theory propounded by Shri. P Chidambaram that may make him a Nobel laureate for Economics. He explored the banking system to be strong enough to bear the burnt of Rs.60,000 Crores without feeling a pinch. And the banking system did not suffer in any way in the process of extending the benefit of loan waiver to defaulters. The fools who repaid loan honestly are people who were made gullible. Long live Chidambaram. Long live his incredible theory. Shri. Reddy had hiccough of a severe nature on the day and hence the magnanimous FM came to rescue him as his mouth piece.

The UFBU secured Pension Option / IBA grants Fresh Option on Pension

“Union is Right, Union is might. Those who did not believe in Unions are in Plight”. It is a great accolade for the UFBU to have achieved a second option on Pension for those who could not opt for it earlier. Many leaders fought for it hard(ly) to see that the lost dream of the bank men is revived and made a reality. Those who blamed the work force who could not opt for it and wanted to see that they never get a fresh chance to opt as also those who categorically declared that CPF was beneficial to the employee are now competing with each other to establish that they fought and won it and are blowing their own trumpets. Will they please clarify:

• Was Pension not an already granted benefit?

• Why did Unions not secure a fresh to those who could not opt for it because of the infusion of the penal clause providing for forfeiture of entire past service in the Final Pension Regulations when the particular clause was deleted from it on 27th February, 2009 through a gazette notification?

• Did any Union or Director representing Workmen or Officers lodge any protest when banks took deviation from the normal procedure of internally issuing a circular about amendment to Service / Pension Regulations (with a statement that it would have effect from the date it is published in gazette) and confined to mere gazette notification for deletion of the penal clause?

• Did the amendment not carry with it an obligation on the part of banks to extend a fresh option? And if so why the issue was not taken up by any one responsible?

• Did any Union or Director know that banks circulated the amendment internally after a period of 43 months? Does the circular not prove that banks were aware of the need for circulating it among the employees and deliberately made a default earlier intentionally? Or did they circulate it belatedly as a measure of time pass?

• Was not a fresh option legally mandatory along with the amendment to Regulation? If so, was Pension not an already vested benefit which the banks unlawfully detained making the work force gullible?

• Why did Pension Option afresh vanish from the charter of demands of different Unions during the period from 2001 to 2006?

• How and why did Unions agree with the IBA during the course of 8th Bipartite Settlement that the item Pension Option would not be opened again?

• How and why did the two schools of thought (one objecting fresh option and the other sticking to the stand that CPF was still beneficial) took somersault from their old barracks and started fighting for fresh option?

• When the Government sanctioned and Board adopted Pension Regulations stated unambiguously that the option once exercised shall be final and irrevocable and the Regulations did not contain a provision for revocation of an exercised option, how did banks revoke the options of some employees at the behest of IBA? Was the revocation legal? Did Unions / Directors not know anything about this?

• Why did UFBU not insist on IBA to conclude the Pension Option issue within the time frame of 3 months as per the MOU dated 25th February, 2008 and caused another 18 months to lapse?

• Even on reaching a second MOU on 7th August, 2009 to give 17.5 percent wage hike and Pension Option why did it did not fruitfully meet the IBA to finalise things until 27th November, 2009? Was UFBU waiting for an auspicious day (the anniversary of a leader) for signing the pact to commemorate the event?

• Have all banks contributed 10 percent of the pay of each employee who joined the Pension Scheme to the Pension Fund of the respective banks as envisaged by the Pension Regulations Chapter relating to the composition of Fund?

• Was there not a provision for contributing a portion of the pay hike to the Pension Fund in the earlier bipartite settlements? Or is it the first time that the contribution formula (70:30) is evolved?

• When a segment of employees including those under VRS are paid full Pension including that on the notional service of 5 years ( which was denied illegally and released as per SC order) will it not tantamount to discrimination when the 70:30 formula is implemented for sharing of Pension burden? Will it not precipitate matters further?

• The Incremental profits of 17 listed Public Sector Banks over March 2006 level was to the tune of Rs.22,502.30 Crores during the ensuing three years . What was the difficulty of the banking system for pleading paucity of funds for meeting the Pension Burden and asking the employees to share the burden of Rs.1 , 200 Crores?

• During 2002 -2006 period public sector banks standing under the common umbrella of IBA were fighting with and pulling the legs of each other for take over of loans from counterparts for mere cosmetics of the key men employing the lethal weapon of interest rates taking advantage of the deregulated interest regime. Interest concessions were extended to potential borrowers while no benefits were given to the deserving. Life blood of banks oozed out in big proportions and banks got debilitated. Unwanted work load of processing the proposals of an avoidable nature was the only benefit to the banks. The vehement criticisms I leveled against those concerned when they extravagantly wasted money in the context of their lame extenuation to extend fresh option on Pension brought an end to the “take over mania” in the latter half of 2006-2007. If I state that my work resulted in making the banking system robust and make profits of a progressive nature from March, 2007, it would be calling a spade a spade only.

• Will the Unions that collected subscription from members throughout their service period cease to have any responsibility towards them when they retire? Are Unions not having any responsibility in respect of implementation of the agreements relating to the post retirement benefits? Were the Unions justified in not helping the retired in getting the terminal benefits correctly and in driving them to the various courts in quest of justice?

It is my earnest desire to give a clap to UFBU on the laudable achievement of Pension Option to the work force and hence I earnestly request any one of you to please clarify on the above points.

Thanks and Regards

C N Venugopalan

According to statistics submitted by the finance ministry before Parliament on Friday, the government banks together in the last three years, since 2007, have written off nearly Rs 25,000 crore. -- Times of India - This could be done splendidly No money to meet establishment expenditure for the bankrupt bankers

Banking System fully loaded with Fake Currency

On 2008 March 6 by the then Finance Minister stated as follows

(Financial Express on 7th March, 2007)

The minister added that RBI governor Y V Reddy has told the board that the central bank was “fully geared to support the government in implementing the scheme in a manner that the banking sector will be strengthened, not weakened.”

This is the new theory propounded by Shri. P Chidambaram that may make him a Nobel laureate for Economics. He explored the banking system to be strong enough to bear the burnt of Rs.60,000 Crores without feeling a pinch. And the banking system did not suffer in any way in the process of extending the benefit of loan waiver to defaulters. The fools who repaid loan honestly are people who were made gullible. Long live Chidambaram. Long live his incredible theory. Shri. Reddy had hiccough of a severe nature on the day and hence the magnanimous FM came to rescue him as his mouth piece.

The UFBU secured Pension Option / IBA grants Fresh Option on Pension

“Union is Right, Union is might. Those who did not believe in Unions are in Plight”. It is a great accolade for the UFBU to have achieved a second option on Pension for those who could not opt for it earlier. Many leaders fought for it hard(ly) to see that the lost dream of the bank men is revived and made a reality. Those who blamed the work force who could not opt for it and wanted to see that they never get a fresh chance to opt as also those who categorically declared that CPF was beneficial to the employee are now competing with each other to establish that they fought and won it and are blowing their own trumpets. Will they please clarify:

• Was Pension not an already granted benefit?

• Why did Unions not secure a fresh to those who could not opt for it because of the infusion of the penal clause providing for forfeiture of entire past service in the Final Pension Regulations when the particular clause was deleted from it on 27th February, 2009 through a gazette notification?

• Did any Union or Director representing Workmen or Officers lodge any protest when banks took deviation from the normal procedure of internally issuing a circular about amendment to Service / Pension Regulations (with a statement that it would have effect from the date it is published in gazette) and confined to mere gazette notification for deletion of the penal clause?

• Did the amendment not carry with it an obligation on the part of banks to extend a fresh option? And if so why the issue was not taken up by any one responsible?

• Did any Union or Director know that banks circulated the amendment internally after a period of 43 months? Does the circular not prove that banks were aware of the need for circulating it among the employees and deliberately made a default earlier intentionally? Or did they circulate it belatedly as a measure of time pass?

• Was not a fresh option legally mandatory along with the amendment to Regulation? If so, was Pension not an already vested benefit which the banks unlawfully detained making the work force gullible?

• Why did Pension Option afresh vanish from the charter of demands of different Unions during the period from 2001 to 2006?

• How and why did Unions agree with the IBA during the course of 8th Bipartite Settlement that the item Pension Option would not be opened again?

• How and why did the two schools of thought (one objecting fresh option and the other sticking to the stand that CPF was still beneficial) took somersault from their old barracks and started fighting for fresh option?

• When the Government sanctioned and Board adopted Pension Regulations stated unambiguously that the option once exercised shall be final and irrevocable and the Regulations did not contain a provision for revocation of an exercised option, how did banks revoke the options of some employees at the behest of IBA? Was the revocation legal? Did Unions / Directors not know anything about this?

• Why did UFBU not insist on IBA to conclude the Pension Option issue within the time frame of 3 months as per the MOU dated 25th February, 2008 and caused another 18 months to lapse?

• Even on reaching a second MOU on 7th August, 2009 to give 17.5 percent wage hike and Pension Option why did it did not fruitfully meet the IBA to finalise things until 27th November, 2009? Was UFBU waiting for an auspicious day (the anniversary of a leader) for signing the pact to commemorate the event?

• Have all banks contributed 10 percent of the pay of each employee who joined the Pension Scheme to the Pension Fund of the respective banks as envisaged by the Pension Regulations Chapter relating to the composition of Fund?

• Was there not a provision for contributing a portion of the pay hike to the Pension Fund in the earlier bipartite settlements? Or is it the first time that the contribution formula (70:30) is evolved?

• When a segment of employees including those under VRS are paid full Pension including that on the notional service of 5 years ( which was denied illegally and released as per SC order) will it not tantamount to discrimination when the 70:30 formula is implemented for sharing of Pension burden? Will it not precipitate matters further?

• The Incremental profits of 17 listed Public Sector Banks over March 2006 level was to the tune of Rs.22,502.30 Crores during the ensuing three years . What was the difficulty of the banking system for pleading paucity of funds for meeting the Pension Burden and asking the employees to share the burden of Rs.1 , 200 Crores?

• During 2002 -2006 period public sector banks standing under the common umbrella of IBA were fighting with and pulling the legs of each other for take over of loans from counterparts for mere cosmetics of the key men employing the lethal weapon of interest rates taking advantage of the deregulated interest regime. Interest concessions were extended to potential borrowers while no benefits were given to the deserving. Life blood of banks oozed out in big proportions and banks got debilitated. Unwanted work load of processing the proposals of an avoidable nature was the only benefit to the banks. The vehement criticisms I leveled against those concerned when they extravagantly wasted money in the context of their lame extenuation to extend fresh option on Pension brought an end to the “take over mania” in the latter half of 2006-2007. If I state that my work resulted in making the banking system robust and make profits of a progressive nature from March, 2007, it would be calling a spade a spade only.

• Will the Unions that collected subscription from members throughout their service period cease to have any responsibility towards them when they retire? Are Unions not having any responsibility in respect of implementation of the agreements relating to the post retirement benefits? Were the Unions justified in not helping the retired in getting the terminal benefits correctly and in driving them to the various courts in quest of justice?

It is my earnest desire to give a clap to UFBU on the laudable achievement of Pension Option to the work force and hence I earnestly request any one of you to please clarify on the above points.

Thanks and Regards

C N Venugopalan

According to statistics submitted by the finance ministry before Parliament on Friday, the government banks together in the last three years, since 2007, have written off nearly Rs 25,000 crore. -- Times of India - This could be done splendidly No money to meet establishment expenditure for the bankrupt bankers

Friday, December 4, 2009

This is an old circular now published in the blog. Time constraints did not allow earlier posting

Dear Fellow Bankers,

Bank Trade Unions are functioning in queer ways. Leaders are working for their own goals. There are two directors ( representing workers and officers) on board different public sector banks charged duty is to function as spokesmen of the workforce. All along, they have been sleeping or clapping hands on all wrong decisions prejudicially affecting workers.

Unions severe the connections with members when they retire. They drove all the retired to different courts for justice without addressing their issues. Many who were denied Pension Option had to approach Courts. Pension matter was a stale one until early 2006 and Unions had, in the course of 8th Bipartite Talks, surrendered the right of employees agreeing not to reopen it again.

Unions started adddressing the issue only after I issued an all India Circular on 10th January, 2006 to all fellow bankmen. ( You can see some items in the blog " www.bankpension.blogspot.com". You may visit the blog and scroll against the different items seen on the left hand side in the blog. ). Agitating for five days on the Pension Issue that was buried deep in the grave yard for years together, the bank unions once again proved that they have power. The MOU dated 25th February, 2008 agreeing to settle Pension Issue within three months from then is the Magna Carta of Pension in the history of Banking. Unions that were averse to Pension in mind did not enforce the MOU even after the anniversary date and allowed to mix it up with wage revision. The reluctant horse was pushed to the pond, but still it refused to drink water. If Pension issue was settled within the agreed time frame or within the next six months it would never have got mixed up with the Wage Talks, giving the IBA a bargain to for employee's contribution for meeting pension bill. Once again, the interests of workforce got pledged. The elephant continues to walk as per the tunes played by the mahout without realising its strength.

Pension becomes contributory for all present employees who will have to surrender Rs.8.00 lakhs to Rs.12.00 lakhs standing to their CPF for joining the scheme. Again, a portion of the proposed wage hike is reportedly contributed towards Pension Burden. After making it contributory for the existing work force, Unions bargain for a non-contributory Pension Scheme for people who are to be recruited in future without any sacrifice or contribution from their side. Is it not strange? Let you be the judge.

I have spent about Rs.3.00 lakhs out of my terminal benefit on Printing Postage and stationery to bring the issue of Pension to the present status. While unions say that they have no commitment or responsibility to retired employees, one retired officer has spent huge money and efforts lasting for eight years to secure Pension Benefit to those working when the unions they subscribe to remained non-performing on it.

Union is strength. Unions in might Union is right. Split among the different unions alone created the issues. Let a change of heart take place among the leaders so that they work for the real benefit of the members

The option is not a second option. As per the present Pension Scheme in operation in Banks ( sans the clause enabling forfeiture of entire past services for participation in strike) no employee has got an option. If the existing Pension Scheme is implemented in letter and spirit, all are entitled to a fresh option which is the "first option" itself. It appears to be ridiculous when one calls it a second option. If they fail to sort out the Pension Issue separately people may start calling them UFBU assigning the expansion"Unscrupulous" for U

Dear Fellow Bankers,

Bank Trade Unions are functioning in queer ways. Leaders are working for their own goals. There are two directors ( representing workers and officers) on board different public sector banks charged duty is to function as spokesmen of the workforce. All along, they have been sleeping or clapping hands on all wrong decisions prejudicially affecting workers.

Unions severe the connections with members when they retire. They drove all the retired to different courts for justice without addressing their issues. Many who were denied Pension Option had to approach Courts. Pension matter was a stale one until early 2006 and Unions had, in the course of 8th Bipartite Talks, surrendered the right of employees agreeing not to reopen it again.

Unions started adddressing the issue only after I issued an all India Circular on 10th January, 2006 to all fellow bankmen. ( You can see some items in the blog " www.bankpension.blogspot.com". You may visit the blog and scroll against the different items seen on the left hand side in the blog. ). Agitating for five days on the Pension Issue that was buried deep in the grave yard for years together, the bank unions once again proved that they have power. The MOU dated 25th February, 2008 agreeing to settle Pension Issue within three months from then is the Magna Carta of Pension in the history of Banking. Unions that were averse to Pension in mind did not enforce the MOU even after the anniversary date and allowed to mix it up with wage revision. The reluctant horse was pushed to the pond, but still it refused to drink water. If Pension issue was settled within the agreed time frame or within the next six months it would never have got mixed up with the Wage Talks, giving the IBA a bargain to for employee's contribution for meeting pension bill. Once again, the interests of workforce got pledged. The elephant continues to walk as per the tunes played by the mahout without realising its strength.

Pension becomes contributory for all present employees who will have to surrender Rs.8.00 lakhs to Rs.12.00 lakhs standing to their CPF for joining the scheme. Again, a portion of the proposed wage hike is reportedly contributed towards Pension Burden. After making it contributory for the existing work force, Unions bargain for a non-contributory Pension Scheme for people who are to be recruited in future without any sacrifice or contribution from their side. Is it not strange? Let you be the judge.

I have spent about Rs.3.00 lakhs out of my terminal benefit on Printing Postage and stationery to bring the issue of Pension to the present status. While unions say that they have no commitment or responsibility to retired employees, one retired officer has spent huge money and efforts lasting for eight years to secure Pension Benefit to those working when the unions they subscribe to remained non-performing on it.

Union is strength. Unions in might Union is right. Split among the different unions alone created the issues. Let a change of heart take place among the leaders so that they work for the real benefit of the members

The option is not a second option. As per the present Pension Scheme in operation in Banks ( sans the clause enabling forfeiture of entire past services for participation in strike) no employee has got an option. If the existing Pension Scheme is implemented in letter and spirit, all are entitled to a fresh option which is the "first option" itself. It appears to be ridiculous when one calls it a second option. If they fail to sort out the Pension Issue separately people may start calling them UFBU assigning the expansion"Unscrupulous" for U

Following the agitations that took place in furtherance of Pension Option, the MOU of 25th February, 2008 to settle the issue within three months from then was signed by IBA and UFBU.

Three months, six months, nine months twelve months and 15 months elapsed without anything happening within the time frame thanks to the yeoman service of the TU leaders.

The independent issue of Pension which was an already conferred benefit and was later taken away from the work force gets mixed up with the wage revision talks giving a leverage to make a foul bargain in the name of the Pension burden and the IBA becomes successful for prolonging the matter. The next agitation takes place on 6th and 7th August, 2009. On 7th August, 2009 IBA makes the offer of 17.50 percent wage hike and Pension Option, the latter on sharing basis in the ratio 70:30 by banks and employees.

Unions that sold out the already vested right to Pension of the employees in 2005 during the course of the 8th Bipartite by agreeing not to open the issue again now agreed to share the Pension burden out of wage hike. The delay made them to move through the dotted lines drawn by IBA and to agree to what they dictated. Now it is funny to see the unions beat their own trumpet on accomplishing Pension. The AIBEA and allies who blamed the victims for not opting for Pension and wanted to see that such people never get a chance again and the BEFI allies who stuck to their stand that CPF is beneficial even on realizing that they were wrong are now competing with each other to make the bank men believe that they made a fabulous achievement. They had leashed justice from reaching the victims and now they take a somersault from the South Pole to North Pole and pretend as apostles of Pension.

Stop weeping mother India. You have such great sons. They behave in their own strange ways.

Three months, six months, nine months twelve months and 15 months elapsed without anything happening within the time frame thanks to the yeoman service of the TU leaders.

The independent issue of Pension which was an already conferred benefit and was later taken away from the work force gets mixed up with the wage revision talks giving a leverage to make a foul bargain in the name of the Pension burden and the IBA becomes successful for prolonging the matter. The next agitation takes place on 6th and 7th August, 2009. On 7th August, 2009 IBA makes the offer of 17.50 percent wage hike and Pension Option, the latter on sharing basis in the ratio 70:30 by banks and employees.

Unions that sold out the already vested right to Pension of the employees in 2005 during the course of the 8th Bipartite by agreeing not to open the issue again now agreed to share the Pension burden out of wage hike. The delay made them to move through the dotted lines drawn by IBA and to agree to what they dictated. Now it is funny to see the unions beat their own trumpet on accomplishing Pension. The AIBEA and allies who blamed the victims for not opting for Pension and wanted to see that such people never get a chance again and the BEFI allies who stuck to their stand that CPF is beneficial even on realizing that they were wrong are now competing with each other to make the bank men believe that they made a fabulous achievement. They had leashed justice from reaching the victims and now they take a somersault from the South Pole to North Pole and pretend as apostles of Pension.

Stop weeping mother India. You have such great sons. They behave in their own strange ways.

Subscribe to:

Posts (Atom)