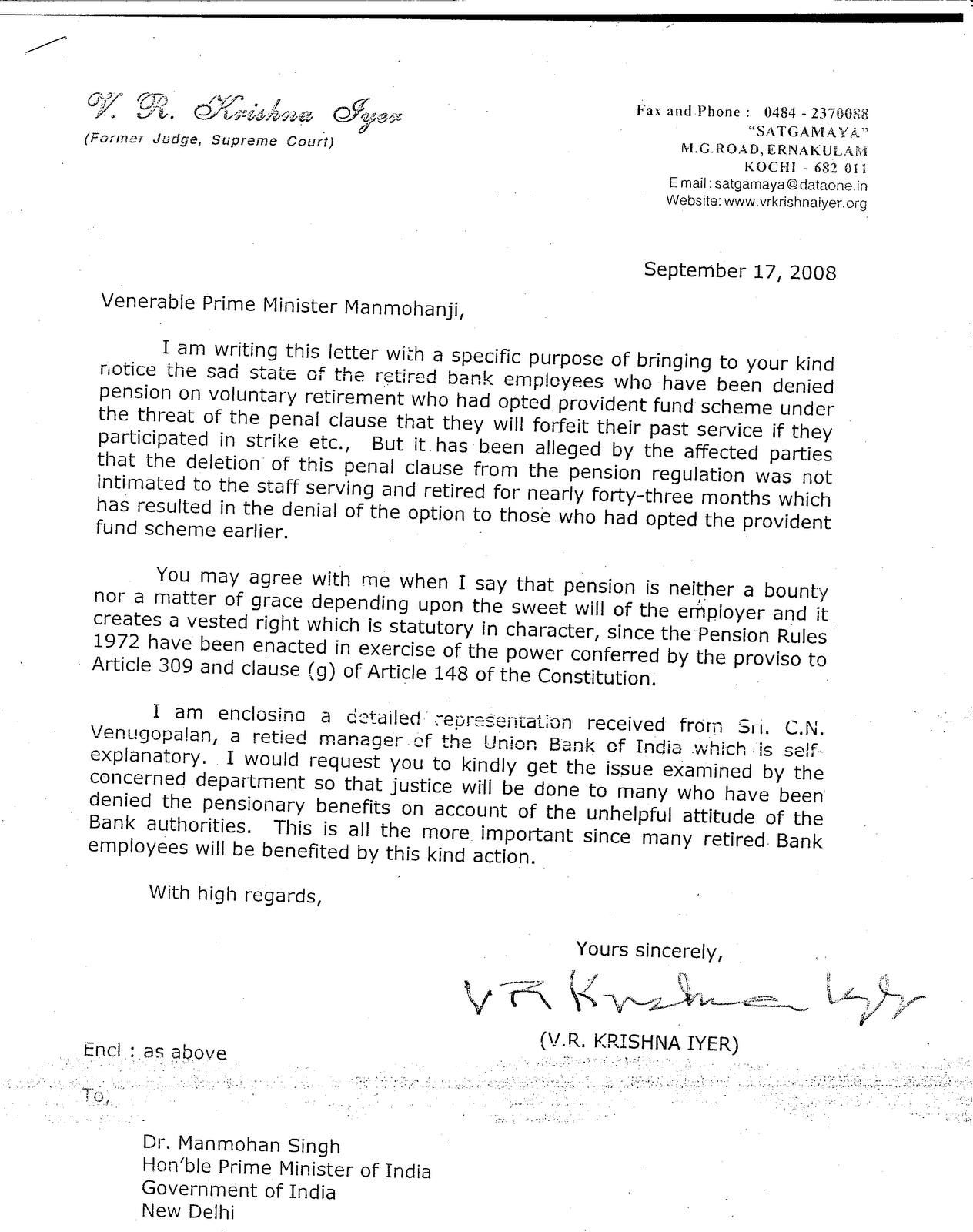

C N Venugopalan

Ex- Manager, Union Bank of India &

Vice President, Union Bank of India Retired Officers’ Association (Kerala)

“ Nandanam”

Kesari Junction

North Paravoor

Kerala – 683 513

Phone No. 0484 2447994 Mobile: 9447747994 e-mail: ceeyenvee@gmail.com

PEN CNV 111/08 3rd May, 2008

The Principal Secretary,

Financial Sector,

Govt. of India,

Ministry of Finance,

New Delhi

Dear Sir,

Sub: Wage Revision in Banks and Imprudent Banks Association (IBA)

With grave concern, I inform you that the Indian Banks Association (IBA ) has, in course of time, proved itself to be the most imprudent organization all over the world by framing and implementing policies and schemes in banking industry. It has functioned in the most undemocratic and discriminatory ways quite inconsistent with the spirit of Indian Constitution. The policies it adopted and schemes implemented engendered gross violation of all principles of equity and equality enshrined in the constitution and thus infringed the fundamental rights of the workmen in the industry. They entered into separated wage pacts in respect of SBI and the rest of the banks conferring distinct advantages to the former by granting higher starting pay. The perquisites and allowances granted to workmen and officers vary from bank to bank with no uniformity, resulting in utter discrimination notwithstanding the fact that all are doing identical work. The uniformity the government envisaged in such matters is totally disrupted. Banks like State Bank of Travancore compensate their staff for working on Sundays and holidays whereas in many other public sector banks, they are forced to work like slaves without remuneration. Extracting work without paying for is a crime, which, such banks are indulging in. Uniform pay for identical work and compensation for all work, unless it be voluntary work done, are things to be enforced on principles of equity. Perquisites granted in banks should also be uniform to meet the requirement of fairness Separate wage pact for SBI and for rest of the banks as also disparity in terminal benefits are items to be done away with, with immediate effect.

IBA has been incessantly doing acts prejudicial to the interest of the bankers and of the general public by discriminating the employees and driving the workforce out of their seats to the streets in protest causing inconvenience to the public through frequent interruption in banking service. It has thus proved itself to be an incompetent body to evolve policies, especially in compensation packages for labour. It committed several absurdities and obtained the approval of the Government for all erroneous schemes. They made unauthorized payments from the system and created fresh law for escaping the accountability aspect arising there from. At their instance, member banks paid to those who retired through VR Scheme, pension from the ensuing month of their retirement in 2001 in spite of the fact that there was no enabling provision in the Pension Regulations for payment of Pension to anybody before attaining the age of superannuation. They threw away substantial amounts with the least intelligent reckoning and subsequently amended Regulation 28 of the Pension Regulations in banks on 13th July, 2002 with retrospective effect stating that with effect from 01 09 2000, pension also shall be payable to an employee who opts to retire through any scheme formulated by the bank and approved by the Government and thus obtained Government nod ratifying the erroneous payments. Can any one classify this as anything else other than imprudence and sheer abuse of authority to cover up one’s own mistakes?

The Voluntary Retirement Scheme evolved and implemented in 2000 was typical of the bedlam IBA and contained illegality, absurdity and totally lacked vision. It perpetrated gross discrimination among the retirees from two segments viz. those whom the banks placed in Pension Stream (Category 1) and those in Provident Fund stream (Category 2). The defects and discrimination run as follows:-

· Category 1 who were otherwise entitled to Pension after attaining the age of 60 only were paid Pension from the next day of retirement

· Category 2 to whom banks should otherwise have paid compulsory PF contribution (employer’s share) up to the age of 60 were denied PF contribution – a retirement benefit - from the next day of retirement

· Category 1 got salary for the left over period of service concurrently with pension for the same period, which is a phenomenon not heard anywhere in the universe

· A good number from the Category 1 secured employment with other banks too and got salary from the new employer also along with pension and salary for the left over service from the erstwhile employer. In other words, they got double salary and pension from the banking system that claims to be ailing and pleads inability to pay pension to the category 2 employees

While making the offer of VRS, its terms vividly stated that those under Pension Segment would be paid Pension as per the Pension Regulations. The Pension Regulations provided for payment of Pension by adding a notional period of five years to the actual service put in for reckoning qualifying service. At the fag end of the period of offer of VRS and without giving a chance to withdraw subscription already made on the basis of the original terms of offer, some member banks of IBA varied the terms of offer stating that the notional period will not be allowed. Member banks thus resorted to foul play, prejudicing the interest of the employees just in the same way children play foul smelling defeat in games, violate all ground rules and spoil the entire game. IBA and Banks took away the sanctity of the process and acted in a silly manner, ignoring the legal requirement of giving an opportunity to withdraw subscription to VRS in the wake of the amended rules. Banks drove the affected parties to different courts of law.

Pension Scheme in Banks and its implementation was altogether wrong in the sense that:-

Banks called for Irrevocable option for Pension from employees categorically stating in the Pension Regulations that option once given shall be final and irrevocable. This was the position as per the draft regulations circulated as also the final Regulations after adoption by Boards of different banks and final approval of the Government. Banks called for option from employees within a stipulated time while publishing draft Regulations among the employees. Subsequently, while circulating the final Regulations also, options were called for within a specified time ( a second date subsequent to that as per draft Regulations) and stating that those who exercised the options earlier need not give option letters afresh. The finalized Regulations contained an additional penal clause apart from those stated in the draft Regulations to the effect that in case an employee participated in a strike any time after joining the Pension Scheme, the bank could forfeit the entire past services of the employee. As such, to the employees with a service of over ten to twenty years, who joined the Pension Scheme by surrendering to the Pension Fund of the Bank, the entire employer’s compulsory PF contribution lying to his credit, participation in a strike would entail loss of Pension as also PF benefit. For this reason, when the banks gave a further chance to withdraw the option for Pension, several employees who opted for Pension originally assented to withdrawal of option. However, Pension Regulations never contained a provision for revocation of options in any of the Regulations. Hence, the communication offering withdrawal of Pension Option, the revocation by employees and the process of revocation are all null and void in the eyes of the law for want of a provision therefor in the Pension Regulations. In case of all who have exercised option any time, the option has to be irrevocable itself as per the text of the option letter and as per the Pension Regulations.

Even assuming that the employees have not exercised options in the wake of the penal clause enabling forfeiture of past service for participation in strike, banks had a liability to exercise fresh option upon deleting the clause in the month of February, 1999 since they could not exercise it on account of the presence of the deleted clause in the Regulations. Not only did they extend a fresh option, but banks , in variance of the usual practice of circulating the proposed amendments in English and Hindi among the employees and stating that the amendment will have effect from the date it is published in the gazette of India confined the publication in Gazette only to keep the target group in darkness about the development. The Government may examine the propriety of this malafide action.

The Pension Scheme itself is entirely bad and unscientific to the extent:

· It now refuses Pension to the employees with twenty to thirty years of service for whose benefit it was brought even against surrender of the entire PF contribution( employer’s share running in Rs.5.00 to Rs.7.00 lakhs) to the Pension Fund. Of banks. At the same time, in the case of fresh employees recruited after its commissioning, it gives the benefit compulsorily even if there is no such contribution or sacrifice from their side. It should encompasses all those who worked for the respective organizations for thirty to thirty five years and are already in service or have quit through retirement, normal and voluntarily

· It took under its purview all those who retired already at the time of its commissioning up to a prior date of 01 01 1986 whereas it denies the benefit to majority of employees who are were in service as on the date of its commissioning, in the name of an option which the employees could not exercise on account of reasons beyond their control (the clause relating to forfeiture of service for participation in service).

· A segment that retired through VRS are given Pension before the normal date of superannuation against their normal eligibility to get it after attaining the age of 60. But the segment that happened to be in PF stream for no fault of theirs are denied Pension altogether by virtue of the wrong implementation of VRS. Whereas both the segments have done identical service, the denial of Pension to one segment is illegal and discriminatory.

As results of labour unrest demanding Pension option afresh, the banking system got paralyzed for three days during 206-2007 and 2007-2008 causing inconvenience to public.

The wage pacts formulated and signed by the IBA with Unions in the industry placed the bank employees on three planes in the matter of compensation for labour notwithstanding the fact that all of them are doing identical work in the field. Reserve bank employees who have mere monitoring role not resulting in any productivity have the highest pay scale and perquisites and have superior status. Next come SBI employees with a slightly lower pay scale and perquisites than RBI employees which is much higher than that of employees in other scheduled banks. The workmen in other banks are given the lowest scale and perquisites. Though the compensation package of the latter two is settled by IBA, there is discrimination of a high order. Again allowances differ from bank to bank since some banks grant their employees special allowances for attending work during late hours and on holidays. These actions are in gross violation of all ethics and principles upheld by the Constitution of the nation and by substantive law.

IBA a body of bankers supposed to be the veterans has proved, through its imprudent and illegal actions, that the office bearers are in mere novicehood by doing things prejudicial to the interest of the bankers and of the general public. IBA is, by going on with actuarial exercise of assessing the liability, now dilly dallying the issue of extending second option on Pension in spite of the legal onus cast on banks in the wake of the amendment to Pension Regulations made in February, 1999 . Though banks plead paucity of money to extend a fair deal to the workers, they have money to squander on granting interest free loans to sugar sector wasting several crores of Rupees and for write off to defaulters in Agricultural sector to please the political masters. Again they have money to spend several crores (Rs.300 to Rs.400 Crores) to spend on items like change of logos. Standing below the common umbrella of IBA, they competed with and pulled the legs of each other by offering reduced rates of interest to potent borrowers on loans taken over from counterparts. The drain on the resources out of the unhealthy and meaningless competition which runs in several thousands of Crores of Rupees is not assessed by the banks or by RBI. The Government has to examine the matters in detail and take proper corrigendum action.

In the larger interests of the bank employees and former employees like me who are badly affected by non-extension of pension option so far, I request that the IBA be directed to grant fresh option expeditiously without wasting time. PF accounts of employees consisted of two portions viz. compulsory contribution of the employer and that of the employees. Out of this, the employer’s contribution up to the date of commencing Pension Scheme was confiscated to the Pension Fund of the banks for building up Pension Fund. Thereafter, banks should have transferred the monthly contributions in respect of those who joined the scheme into the Pension Fund to build it up well. But they did not do so and took the amount of committed establishment costs as profits. The amount so converted can be assessed by taking the current values in the employee’s share of PF and reducing from it the amount transferred to pension fund in respect of the employee in the year 1995. Banks have to bring in funds to this extent to Pension Fund so as to scientifically assess the actuarial value of the pension Fund. If such an exercise is done, there will be surplus funds for meeting the pension obligation of all since the Pension Fund will be augmented by fresh contribution of PF balance of those who are to join the scheme.

In granting the second option on pension it has to be considered that RBI extended to its employees a fresh option in the year 2000. In government organizations like the railways, options were extended for 12 to 14 occasions with every change in the Pension rules. Now that the banks are delaying extension of pension options to all those who were on the rolls at the time of commissioning the scheme, and are up to considering different modalities for it when already one scheme is in operation, the Government is requested to issue appropriate directions to IBA to rectify the mistakes that are brought to their notice and to enrich themselves as a worthy organization. In view of the unscientific steps they take every time when wage pacts are revised, it is necessary that a pay commission for banking sector to be headed by some legal luminaries like High Court Judges which has no bias of any kind be constituted for the banking sector, taking out the function from the IBA..

Being badly affected by the action of my erstwhile employer in not granting me pension option and pension, in my capacity as an ex-employee and as a member of the general public put to inconvenience through occasional interruption in banking services resultant on the unscientific, incompetent and mad policies of the IBA, I request you to inform me reasons, if any, as to why a petition should not be filed before an appropriate court seeking a direction for debarring IBA from discussing wage talks in future and for directing the Government to appoint a Pay Commission for Banks as in the case of Government employees. MOF may please examine the issue swiftly and let me know within a fortnight since I am planning to file the petition in the opening Court. Also return the acknowledgement copy to me duly acknowledged as it is meant for filing as annexure to the proposed petition

Thanking You,

Yours faithfully,

C N Venugopalan

Acknowledgement copy

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment