Wednesday, September 24, 2008

Letter to Shanta Raju

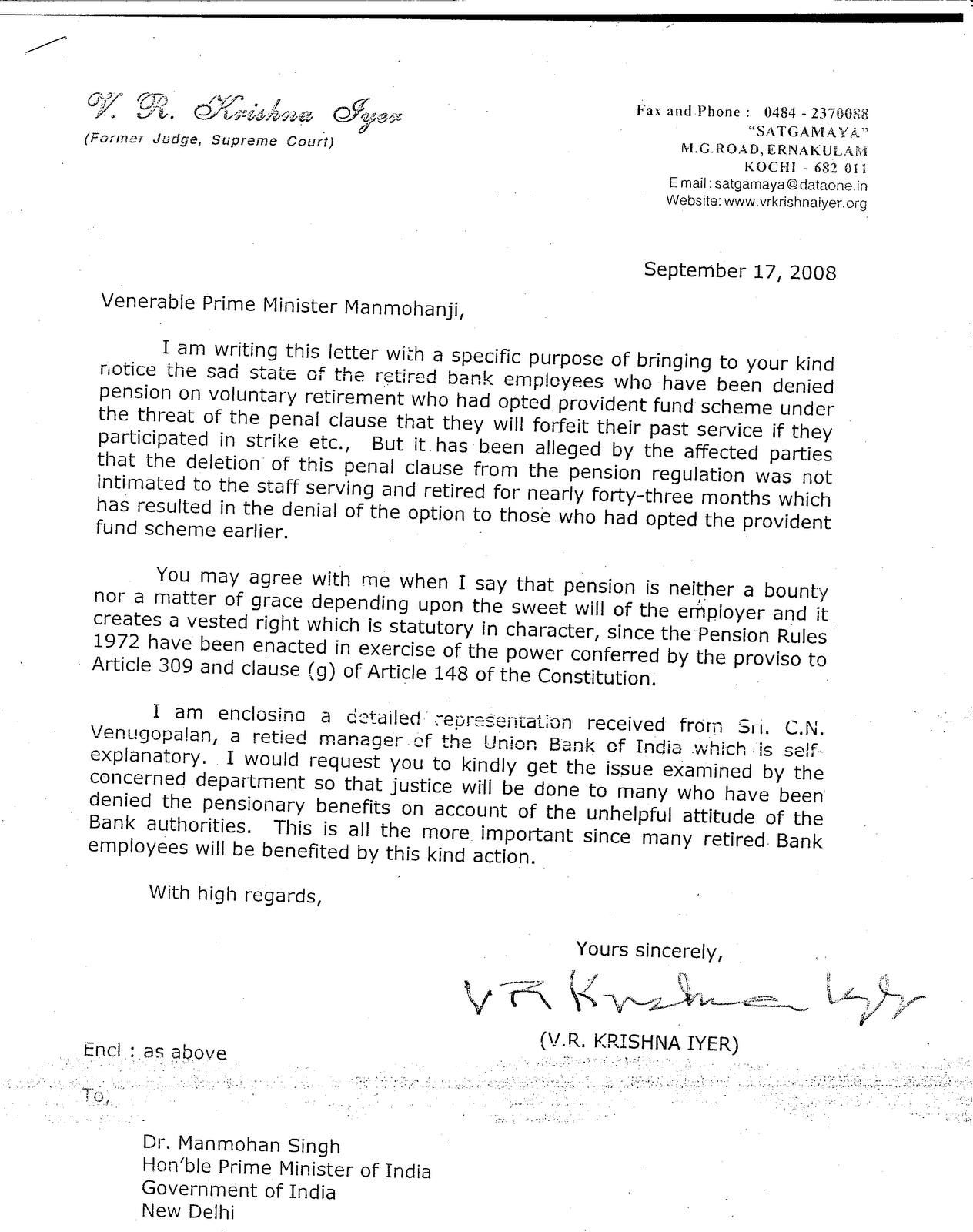

C N Venugopalan

Ex- Manager, Union Bank of India &

Co-ordinator of PF stream bank staff

“ Nandanam”

Kesari Junction

North Paravoor

Kerala – 683 513

Phone No. 0484 2447994 Mobile: 9447747994 Email: cnvenu@yahoo.com

The General Secretary, 12th March, 2006

All India Bank Officers’ Confederation,

P B No. 5160,

State Bank of India Building,

St. Marks’ Road,

Bangalore – 560 001

Comrade,

Addison stood up to repeat in the House of Commons “ I conceive”, “I conceive”, I conceive”. Right Honourable Srinivsa Sastri stood up and said “ Addison conceived thrice but brought forth……… .” One has to say, the veteran Trade Unionists in the Banking Industry who conceived the long pending issue of Pension long long back miserably failed in delivering goods in spite of the lapse of about seven years of conception.

The issue of Compassionate Appointment became ripe for agitation since the Trade Unions had given sufficient warning to the Government and to the Managements not to meddle with the issue. The issue relating to extension of a fresh Pension Option in Banking Industry was not as mature enough as ‘compassionate appointment’ to be pressed upon though Unions conceived it about some seven years back. The Confederation is however quite conscious of the sentiments of the rank and file and their anxiety to see the resolution of the “long pending issue of pension”. Trade Unions got the “forfeiture of Service for Participation in strike” clause scrapped from the Pension Regulations of Banks in February 1999. But they conveniently forgot to secure a chance for fresh option to those who did not join the Pension Scheme because of the existence of the particular clause. The only analogy is that of a dog meddling with a coconut with husk over it. Several of the retired employees in the PF Segment who toiled through and through for the Banks they served died without getting the Pension they were entitled to. Is Pension a consideration for an option exercised? Is it not the consideration for the services rendered? Is it a mischief to urge for a fresh option? Is it proper to call others as mischievous elements after perpetrating mischief? Don’t we have a prick of conscience in the matter? In spite of two wage revisions that took place in the industry after the scrapping of the “Forfeiture of service” clause, was the issue deliberated properly in its true perspective? Though a nation-wide strike was called upon for 9th March, 2006 for demanding the items, both came out as “stillborn children”. AIBOC the trade union “accountable to a large number of Officers across the country having overwhelming majority in the Banking Industry and considered as the sole bargaining agents in almost all Commercial Banks” will however pursue the issues vigorously and achieve it. Thank God. We can rest assured and sit quiet without indulging in cheap gimmicks detracting the Confederation. The confederation,” the sole bargaining agents” is now (but was not in the past) in the right direction and is confident of resolving the issue through UFBU at apex level.

The excerpts of the agreement signed on 2 6 2005 by all the Unions to the effect that IBA reiterated its inability to extend the present Pension Scheme to those who had not opted earlier for various reasons and both the parties agreed to discuss alternative proposals .is also quite reassuring. Why we should have an alternative proposal? How Banks would have met the costs if all the people had opted for Pension when the offer was made? Pension is definitely a consideration for services rendered and not that for an option paper given. Didn’t Banks have a statutory obligation to extend a fresh option when the terms of offer of Pension underwent radical change? Are AIBOC, BEFI etc. not having any role in making members not opting for Pension when the offer was given originally? Have such Trade Unions not done any mischief in making them remain in PF stream? Did RBI not extend a fresh option to its employees in the year 2000? Does RBI make profits to meet the Pension obligations arising out of the second option or will they mint the required money by themselves? Are commercial Banks at present not making good profits to meet the Pension obligations? Is Pension Payment not legitimate establishment expenditure to be fully provided for to ascertain the real profits the Bank makes? Do the general laws applicable to the Country not bind the Banks? All these questions well deserve wise answers from a Trade Union worth its name and fame.

Legal Onus

It is legally established position that when the terms of a tender are revised materially, each bidder should be given a fresh chance to bid. In the case of Pension option, when the deterrent forfeiture of service for participation in strike clause was scrapped from the Pension Regulations in 1999, the Banks categorically had a statutory onus to extend a fresh option to those who did not opt for it earlier. The Constitution Bench of the Supreme Court has made it clear that “Pension is not a charity doled out to the retired employees, but it is their legitimate and inalienable right earned by the sweat of their brows”. (Nakara Case – 17 12 2002). Does the law of the Country not bind the Banking Barons? We are all aware that the IBA publishes all legal decisions affecting Bankers in its journal for benefit of the member banks. Why are they not showing the wisdom to honor the legal obligation cast upon them? Why Trade Unions are shy in achieving the statutorily vested right for their members/ erstwhile members who have made substantial contributions to the banks and the Unions? Have they not encompassed in the Pension Scheme which was commissioned in Banks in 1995 all those who had retired since 01 01 1986 i. e. a decade back for the sake of ensuring Pension to a Tharakeshwar Chakraborthy?

Do Banks run any additional costs through extending a fresh option?

The answer is certainly a big “NO”. The Banks absolutely run no additional costs in extending Pension Option afresh. They had a future liability to contribute to the PF of all the employees on their rolls as of 1995 till their retirement. The PF liability was already a committed and existing one. In the case of those who opted for Pension, Banks ceased to make PF Contributions. In all fitness, the amounts so payable till date of their retirement ought to be notionally worked out on yearly basis and ploughed back into the Pension Fund. The exercise has to be carried out for about 10 years in the past. In the case of those who joined after commissioning of the Pension Scheme also, Banks have to make similar contributions to Pension Fund as otherwise the pay and allowances given to them reduces itself from what was payable otherwise inclusive of the PF Contribution. These facts have escaped the attention of all. When a fresh option is allowed, the PF contribution standing to the credit of such new entrants will also go to augment the Pension Fund. When the future contributions to such employees also are reckoned notionally and transferred to the Pension Fund, the Fund will have surplus not only for paying Pension but also for giving some bonuses. Moreover, after joining the Pension scheme, all are not going to retire the very next day. Moreover, when pensioners die and the family pension also ceases, the pension liability gets reduced too. It is not always an ongoing one. The suggestion for an alternative Pension Scheme is thus absurd and ridiculous. Banks are now robbing Peter to Pay Paul by not accounting the establishment expenses properly and distributing unduly inflated profits as dividends.

ADDITIONAL PAYING CAPACITY

Banks definitely have abundant capacity to contain any additional burden. All Banks are making fantastic profits in spite of the high establishment costs. They are in an age of competition and the Key Men of Banks are resorting to unscrupulous measures to boost their image ( performance) through mere cosmetics. The approach is Penny-wise and Pound-foolish. On one side, we see them sharing ATMs and entering joint ventures for reducing costs. At the same time, for boosting the performance, they resort to drain out profits of the Banking System for catching business by pulling the legs of one another. If IOB has granted a big advance at 12 percent, Indian bank reaches the customer with an offer of 11 percent interest. Now comes Canara Bank with a still reduced interest. Bank of Baroda has a still attractive rate. In spite of all the gimmicks, Banks like Syndicate Bank, Indian Bank, UCO Bank etc. which were ailing earlier also have not only turned corner but are showing fantastic working results. Ground Rules and Code of Business ethics have no place though Banks join hands at IBA and the RBI also is totally unconcerned about the dirty games. The Banking Barons have resources to drain out of the Banking System several Crores through extending interest concessions and write offs to big shots and people with bargaining power. Still they are apprehensive of resources for meeting legitimate establishment expenses. To facilitate the visit of a top executive to Sabarimala or for attending the marriage of a VIP, there is provision to spend lakh to hold a meeting of the Branch Managers at one or two nearby centers. The Salary of all participants and their Traveling Expenses go a sheer waste besides causing inconvenience and trouble for the entire customers. Though Banks have money for such things, they do not have money to pay Pension. Since they lack paying capacity, while entering into Wage Revision Pacts, they determine a load factor and beg back a portion of it for meeting Pension Obligations. The residue is distributed among PF Optees and Pension Optees uniformly with the result that the former category suffers during each Pay Revision. Thanks to Trade Unions, Thanks to Managements. God Pardon them. Their servants pardon them. They know not what they do.

Trace the Culprits

Who are really responsible for the plight of those who remained in PF Stream? There is little or no doubt about it. They are their own counterparts in the other segment who apprehend loss of existing Pension. Trade Unions that advocated PF Options to those with ten years or more of residual service too have an equal role in it. Though prick of conscience cannot go they hibernated over the seven years old problem and miserably failed to accomplish the basic right of their members in spite of the legal, moral and social backing the issue has. The status of the issue is different from Bank to Bank and it has no significance in banks like SBI.

Need of the hour

Let the bygone be bygone. The Confederation which is the sole bargaining agent in most of the Indian commercial banks has started taking the issue in its right perspective and it has the determination to chalk out the right solution to the long pending issue which was not ripe for pressing until now. Let us achieve our legitimate right for the serving and the retired and give up the differences forever.

With regards and Best Wishes, I remain.

Yours comradely,

C N Venugopalan

Subscribe to:

Post Comments (Atom)

1 comment:

who cares for whom and who shares for whom , it is great to read and recall the event 1995.soooo well described

highest regards

m m l gupta

ubi

Post a Comment