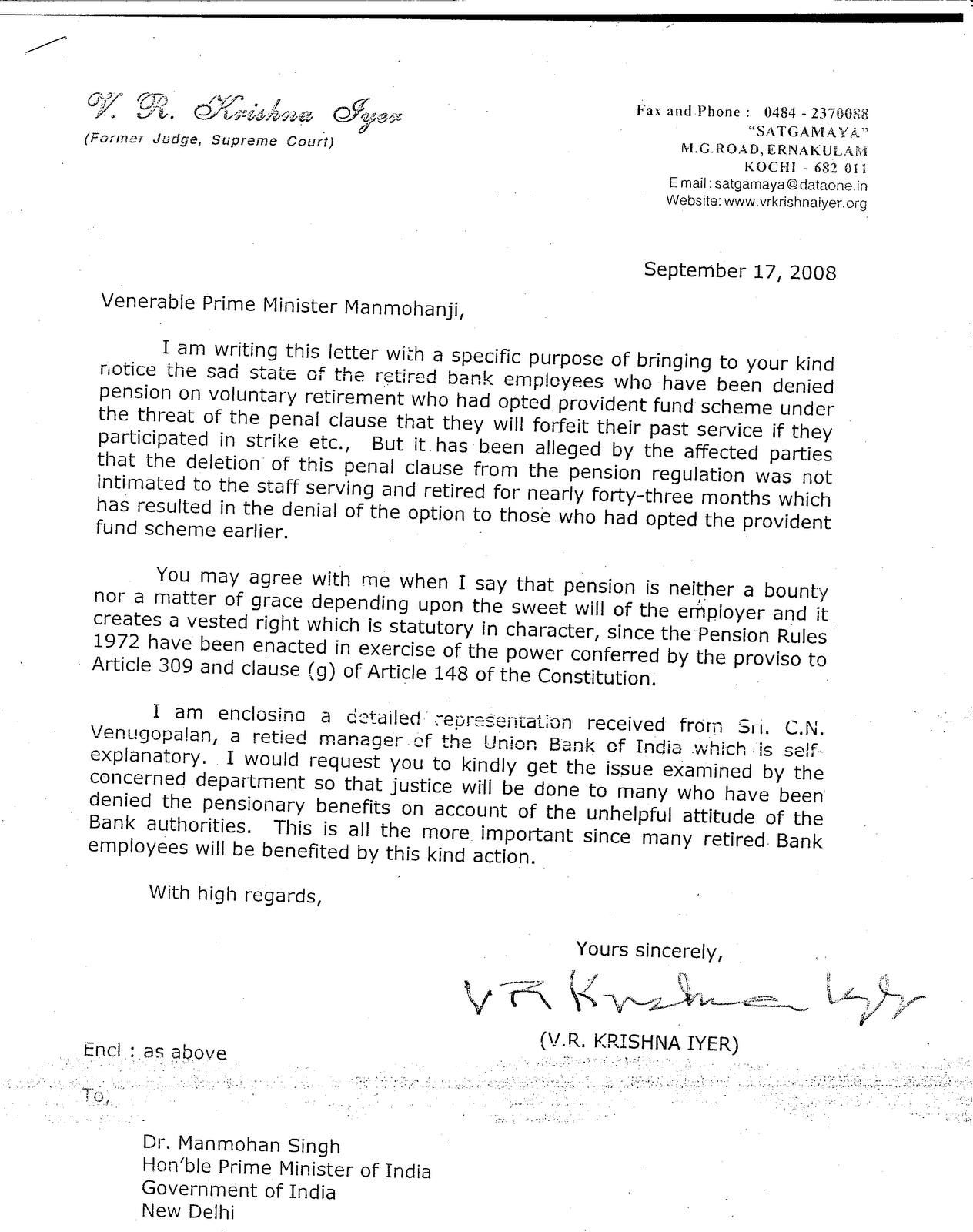

Thursday, September 25, 2008

Letter to Shri. M B N Rao Chairman IBA

C N Venugopalan

Ex- Manager, Union Bank of India

“ Nandanam”

Kesari Junction

North Paravoor

Kerala – 683 513

Phone No. 0484 2447994 Mobile: 9447747994

PEN IBA :123

14th September, 2007

The Chairman,

Indian Banks Association,

For Personal Attention of Shri M B N Rao

Mumbai

Dear Sir,

Be on terra firma, Bankers

I take the privilege of addressing to the Chairman of IBA, ‘house of intelligentsia of Indian Bankers’ that is committed to taking the Indian economy to heights day by day are taking the bank menfor ride. I introduce myself as an erstwhile minute particle of the vast ocean of banking, having voluntarily retired from a public sector bank, more precisely from Union Bank of India, with twice the qualifying service for Pension, yet devoid of it. Since you are heading IBA, the team of experts that claim to be a forward looking organization committed to the progress of the country, I take the privilege of placing before you certain puzzling and riddling facts for treating with your wisdom and for evolving befitting solutions with courage and righteousness without leaving your house as a bedlam.

My observation is that the rich Indian banks have morally turned bankrupt sans a positive mindset and pleads want of capacity for adequately compensating for work while they have ample money to recklessly squander. They imbibe the evils of bureaucracy in its worst form. Even as they derive their powers out of and owe their existence to substantive law of the nation, they utterly disregard all jurisprudence and the provisions of the law and of the Indian Constitution. They spend lavishly on travel, hotel bills, and cock tails accompanying business meetings and customer meets. Lack of integrity and foul play often surface at top levels. In spite of availability of solid securities, they free the loan defaulters extending OTS benefits and release securities for personal ends. The recent news in the air being the graft charge against former CMD and the Regional Head, Ernakulam of Vijaya Bank points to nothing else than corruption and lack of integrity at higher levels. The Chief Executives of Banks which shared ATMs for cost reduction, who are the members of the same house IBA pulled the legs of each other and spent lavishly for each one’s cosmetics in the name of business promotion. CASA is one powerful weapon in their hands to exploit the community to raise interest free and low cost funds without compensating the customers with whose money they flourish. And they beat them severely with exorbitant service charges extended to all possible areas.

The interest concessions given to the potential borrowers in the process of taking over accounts from counterparts made the Indian banking system lose its life blood immensely. Corrupt practices helped potential borrowers to obtain credit at astonishingly low rates. Clever bankers found it a way to get rid of bad accounts by issuing clean chits to defaulting borrowers and helped them take higher level of Credit limits from others banks. This was in full swing until August, 2006 when the Government gave some guidelines on this score. The extent of loss through interest reduction on loans and advances ran in several crores the volume of which is not known to anybody. Despite everything the industry has now become vibrant. Banks which were in the red earlier are posting bright and fantastic working results. Vehement criticisms I made in the second leg of 2006 put the foul games to an end to some extent when the government issued certain guidelines on “interest rate war”. About 10 to 15 percent of the interest income of the entire banking industry during the last year can reasonably be attributed to the efforts I made though everyone concerned will be reluctant to admit. It is my contribution to the entire industry which goes without acknowledgement. The BRA was amended by in August, 2006, changing the nomenclature of their directors on Board the different banks from “Working Directors” to “Nominee Directors” as a result of my criticism that RBI remained a silent spectator to everything. Since February, 2006, I had specifically pointed out to RBI and MOF about the disappearance of a PSB viz. New Bank of India form the banking galaxy despite close supervision and surveillance by the RBI with its directors on Board. When the catastrophe arose, RBI emerged out for saving its face by merging the entity with PNB and went back to pavilion. The entire problems that cropped up and the loss was absorbed by PNB. The queer scientific ways in which many a scheme was implemented in the industry have been quite elusive to me. It is my earnest belief that being the head of the body of bankers that formulates and implements innovative schemes, you are the apt and only person who can solve the riddles and puzzles that appear before me and to clarify the rationale behind the various actions.

In labour scenario, there had been two agitations – one of 27th July, 2006 and the other on 27th October 2006 - pressing the demand for Pension Option afresh in the industry. Another agitation programme scheduled from 28th March 2007 was stalled on the understanding that unions in the industry would submit a scheme before 30th April, 2007 and that a logical conclusion would be made before 30th June, 2007. In this context, what exactly was the reason for another strike in the industry on 12th September, 2007 which has also been stalled? When a Pension Scheme that prescribes the minimum qualifying service and other modalities is already in operation in banks, is there any justification in calling for and considering a fresh scheme. If a MOU had been there, who is at default and who has violated it? Whereas there is a legal onus of extending the existing Pension Scheme to all those having the prescribed qualifying service in the wake of the Feb.1999 amendment to Pension Regulations, what is the justification for wasting time on unnecessary meetings and discussions? It is high time that the motley crowd of experts from the management side and from trade unions enjoying a piggy ride on the back of the work force to stop the foul game and act on realities.

Those who clamour for fresh option are people who could not opt for it earlier when called upon to do so keeping the clause enabling managements to forfeit the entire past services for participation in strike even for a single day as it would deprive them of both PF and Pension after surrendering the CPF to Pension Fund. When Banks scrapped the clause through a Gazette Notification in February, 1999, they had a legal liability of extending a fresh option to such people. Banks, which used to issue internal circular both in English and Hindi, mentioning the details of the proposed amendment for the information of the target group mentioning that it would have effect from the date it is published in the Gazette kept the information in camera by confining to Gazette notification alone. A school boy as well as a legal luminary will not differ in concluding that banks acted malafide in doing so. The stand of the intelligent bankers who find justice in it is analogical to patching a hole with darkness. Once again, when the minimum qualifying service of 20 years for pension was reduced to 15 years in 2000, similar liability arose in the respect of those who did not opt for Pension for want of total service of 20 years ( past service and future service), but with total service of 15 years and more. Can you just explain the justification or rationale behind the action, if any, in not extending fresh option at this point of time for my information? Can it be called by any other name than “Cheating” one’s own folks who brought the banking system to what it is? The so called eminent bankers, when they end up their jobs to live peacefully, will carry with them Balance Sheets that containing imbalance alone. The liabilities in it will certainly overweigh assets or there will be no assets at all left on account of the prick of conscience for having deceived their own folks who worked for them.

The Pension Scheme commissioned in the year 1995 took under its purview all those who retired from 01 01 1986 and paid Pension to all those who had gone out some nine years back by taking back the PF amount paid to them along with a nominal interest. What is the relevance of the effective date 01 01 1986 and was it not to extend the benefit to a trade union leader who retired some time in 1986? If it can be extended to a trade union leader who spent most of his time in organizing the workmen rather than working for the bank, why can’t the benefit be given to those who are working at present and those who retired with the prescribed qualifying service after commissioning the scheme?

The Pension Scheme guarantees a Pension to all those who joined the Banks after its implementation without any sacrifice or contribution from their side to the Pension Fund in the form of surrender of the CPF. Is there any logic behind denying the benefit to those who have already put in service ranging from 30 to 35 years and who would surrender substantial sums lying to the credit of their PF for joining the Pension Scheme? Can it be called by any name other than absurdity of a Himalayan proportion?

Banking intelligentsia that has bureaucratic power and money power ratified several irrational actions to get rid of accountability arising out of all their mistakes. For instance superannuation pension was payable only on attaining the age of superannuation to an employee. But banks paid Pension to all those who took Voluntary Retirement from the ensuing month of exit without the Pension Regulations containing an enabling clause. Regulation 28 was subsequently amended on 13th July, 2002 as follows:

Provided that, with effect from 1st day of September, 2000, pension shall also be granted to an employee who opts to retire before attaining the age of superannuation , but after rendering service for a minimum period of 15 years in terms of any scheme that may be framed for such purpose by the Board with the approval of the Government.”

The said amendment made with retrospective effect, by itself, speaks for want of provision in the Regulations to pay the Pension from the ensuing month of retirement. VRS scheme had stated that those retiring will be paid Pension as per Pension Regulations i.e. from the date of normal super annuation, but banks paid them Pension much earlier contravening the Pension Regulations as well as the V R Scheme. Banks duped those who retired through VRS from the PF segment by depriving them of the PF contribution that was payable to them till the date of super annuation. Those in PF segment have also rendered the same contribution to the industry as that given by the Pension segment people. Can we term the discrimination as banking jurisprudence? Why is the generosity to one segment of people when both the categories have done the same work in all respects? Can you just imagine for a while, to be in the place of a person like me who has rendered ardent service for a period of thirty years, and yet devoid of Pension when the qualifying service to earn Pension in the industry is only 15 years ( just one half of the service I put in) as per the Regulations? The whole English language does not seem to have an apt word to describe the intensity of the hoodwinking involved.

People who embraced Voluntary Retirement are martyrs who made a further sacrifice by surrendering their future services when the banks wanted to trim their size for enhancing working results. They co-operated with the management and accepted a sacrifice which was capital forbearance to them. Is it the mode of exit or the service rendered that qualifies a person to Pension, which is considered as deferred wages akin to fundamental rights guaranteed by the Constitution? Or does the banking jurisprudence contain only wild justice that can deny Pension to subsequent retirees especially in the background of having took under its purview all the retirees with retrospective effect of nine years from 01 01 1986? Is it not quite ironical and strange?

It is pertinent to point out that after taking exit through VRS, a number of people have joined other banks and are working there. The former employer pays him salary for the left over services concurrently with Pension. They are also drawing salary from the Banking system simultaneously. What they need to take is just a permission from the former employer to work again, which is normally given by the Lords in the industry who profess themselves to be above the Supreme God. Is there any logic behind extension of triple benefits to one segment and denying everything to others?

The profits banks generate go to augment the exchequer of the country for paying Pension to the government staff whose work is not linked to any productivity. The politician, who sits for a term of two years either in Parliament or Assembly, despite being ousted on account of serious offences or public disapproval, too earns a pension. The daily bread of a retired bank man is snatched away keeping him to starve for feeding others who have not made any contribution to the industry. Banks are venturing out for the welfare of the world at large without setting right their own house first. Even pimps in the society would feel and mentally consoled elated for their work if they come to know that the bankers are acting in such a mean way.

Conversion or dealing in other’s money is recognized as taboo in banking sector. Banks however did it all along after 1995 by discontinuing all further PF contributions in respect of employees who joined Pension Scheme in 1995, after transfer of their PF balances into the Pension Corpus. Banks which had liability to contribute to CPF in respect of all the employees on the rolls till their retirement conveniently reduced their establishment expenses by discontinuing PF contribution in respect of those who joined the Pension Scheme. Similarly, in the case of fresh recruits after inception of Pension Scheme, the CPF payable was not worked out and transferred to Pension Corpus. Banks converted establishment expenses into profits and distributed as dividends, deceiving the entire work force for past 11 years. Conversion which is an illegal act is practiced and made the order of the day in banking scenario.

The material things to ponder upon are whether Pension is a consideration for a mere letter of option given or one for the relentless, long and efficient service rendered to the organization. The Apex Court has held that:

It is deferred wages and a payment of the compensation for services rendered.

It is not a bounty or a matter of grace depending upon the sweet will of the employer

It created a vested right which is statutory in character because Pension Rules are enacted in exercise of the powers conferred by proviso to Article 309 and clause (5) of article 148 of the Constitution

Pension is not an ex-gratia Payment but it is a payment for past services rendered

It is a social welfare measure rendering socio economic justice to those who in the hey day of their lives carelessly toiled for the employer on an assurance that in their old age they would not be left in the lurch.

The IBA that claims to be a scientific body that aims to bring about progress of the economy has all along been a party to discrimination. It created among the bank men doing the same work, different segments with entirely different compensation packages for labour. It extended distinct advantages to SBI staff by signing separate wage pacts in respect of SBI and the rest of the banks from time to time and uprooted the essence of the Indian Constitution that guarantees equity and Equality as Fundamental Rights. This is the major contribution of the IBA to the country when it is celebrating the Platinum Jubilee of Independence. IBA made a vague jumble of the entire things. SBI people now have two retirement benefits in addition to Gratuity viz. Provident Fund and Pension and the rest in the Industry have only one. RBI employees whose are doing mere monitoring role without their work having any direct productivity are also getting a Pension since RBI extended an option for Pension to them in 2000. IBA is now the single party at default leaving the work force in other banks in the lurch.

Can any one see so many blunders in any other industry? The history of Indian banking can never pardon the conductors of the industry unless they refine themselves and render justice to those who sacrificed their entire career at the altar of the organizations. Extension of fresh option for Pension in its original form without deviations is the one and only permanent solution to garner industrial peace. You now have the option to correct the past mistakes of IBA and make it rest on solid foundation or to continue the sinful show as at present in the most vulgar form. It is my earnest desire that you will spare some thoughts over the issue and settle it in a befitting way to bring it to a logical conclusion and to garner industrial peace and uninterrupted service to the public. Either way, I will have material since I am venturing shortly into the publication of a media item with a team of experts that can excavate and bring to light the various (im)prudent banking stories to run parallel to the “Indian Banker”. Those narrated herein can be elaborated into wonderful pieces and thanks to the Right to Information Act, regular collection of materials to ensure a perennial supply of material concerning write offs, renovations of offices with ulterior aim, tenders etc can be had. The tall claims put forth in the Indian Banker can be examined with facts and figures in it. The CPIOs of banks will also have good work collecting the information relating to write off, securities released in the process etc. from the lower offices and supplying to my team.

With regards, and thanking You, I remain.

Yours faithfully,

C N Venugopalan

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment